Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Preparing for Your Listing Consultation

At the start of this Seller Orientation, we want to give you some information about what you can do before your listing consultation that will help you and your agent have a more productive meeting. At your consultation, your agent is going to be asking you questions about your understanding of the process, your goals for selling your home, and any questions or concerns you may have related to your sale. Your agent will also prepare materials for your review, including an overview of our marketing campaign, an explanation of our service philosophy, and a comparative market analysis to show you what is selling (and not selling!) in your market area.

At the start of this Seller Orientation, we want to give you some information about what you can do before your listing consultation that will help you and your agent have a more productive meeting. At your consultation, your agent is going to be asking you questions about your understanding of the process, your goals for selling your home, and any questions or concerns you may have related to your sale. Your agent will also prepare materials for your review, including an overview of our marketing campaign, an explanation of our service philosophy, and a comparative market analysis to show you what is selling (and not selling!) in your market area.

You will have a more productive meeting if you do a few things in advance. Here is a short list of some of the things you should keep in mind as you prepare for your listing consultation with your agent. You have no obligation to do any of these things, but you’ll find that most of them will help you prepare yourself:

First, you should think about issues involving your home that could affect its showing, marketing, or delay your closing:

•Have you had any work done on the home since you purchased it? If so, do you have the updated certificate of occupancy demonstrating that the work was done in compliance with building codes? If not, issues concerning your “C of O” are likely to delay your closing.

•Do you currently have a STAR exemption on your property taxes that are reflected in your tax bill, and have you grieved your taxes since you purchased the property? That is information your agent needs when marketing the home.

•Can you think of any special showing considerations your agent should be aware of, things like pets, young children, or anyone else who might be living in the home and inconvenienced by showings? If so, let your agent know so he or she can put together specific showing instructions for other agents.

•Do you have any alarm systems in the home that you will be turning on while your home is on the market? If so, make sure your agent has contact information for the alarm company, and your alarm codes.

•Can you think of any relatively dangerous conditions in the home or the exterior, things like steep stairs , uneven flooring, or tripping conditions in the backyard?

•Do you have any valuables that you will need to keep safe for showings and open houses? If so, discuss with your agent how you should protect them.

•Very important: are there any light fixtures, appliances, or window treatments that are attached to your home but which you would like to take with you when you leave? If so, you need to let your agent know so they can be excluded from the sale.

Second, it would be helpful if you started to gather some information and documentation that you will need for the marketing and sale of your home.

Even if you are not certain you are going to list during the consultation, you will eventually need all these things anyway, so you might as well get them together as early as possible. Here’s what you need:

•An extra set of keys to the home, so that your agent can quickly start setting up showings and attach your lockbox (if you want one).

•Your most recent mortgage statement, tax bills, and utility bills, which are helpful in assessing your situation and marketing the home.

•Your paperwork from your purchase, including your deed and contract, which you will eventually need for your attorney.

Finally, we would ask you to think about some important questions that should come up in your listing consultation with your agent:

•What is your time frame? How soon do you need to be moved out, and how soon do you hope to be moved out?

•What are your expectations for your agent? Have you had bad or good experiences with real estate salespeople in the past, and what are you looking for now?

•Where are you moving to? If you are relocating to another part of the country outside our market area, we can help set you up with a great agent to assist you.

•Finally, what are your contact preferences? Some clients like to hear from their agent every day, some every week, some only when there is news. And some like text messaging, some email, some phone, some only like to talk in person. Let your agent know how often you want to communicate, and how.

Homes in Northern New Jersey Are Cheaper Than They’ve Been in a Generation!

Right now is a really great time to be buying a home in Northern New Jersey

Man, do I hate saying that. As I’ve explained before, I hate the phrase “great time to buy,” for a couple of reasons.

First, people have different needs, and a market that’s great for one person might be terrible for another person.

Second, while markets tend to move together, we do see micro-markets (i.e., towns and villages) that defy larger trends. So while it might be a great time to buy in Village A, it might be not so great in Town B.

Third, and most importantly, though, “it’s a great time to buy!” just seems like a hack thing to say, the kind of thing that TERRIBLE real estate agents have said for generations to get unsuspecting and gullible people to buy an overpriced home. And I think that most people get suspicious when real estate agents talk like that.

So I understand if you’re skeptical. And that’s why I don’t want to just TELL you it’s a great time to buy, I want to SHOW you why it’s a great time to buy.

Specifically, I want to make this specific point: the monthly payment you need to buy an inflation-adjusted average priced home in Northern New Jersey is as low as its been in a generation.

Think about what I’m saying for a second. I’m NOT saying that homes are cheaper than they’ve ever been. That’s not true. Depending on the year, homes have appreciated, and if you go back more than 15 years, they’ve appreciated pretty dramatically. I’m just saying that the MONTHLY PAYMENT you need to make to buy the AVERAGE PRICED HOME is lower right now than it’s been in a generation — if you control for the effects of inflation.

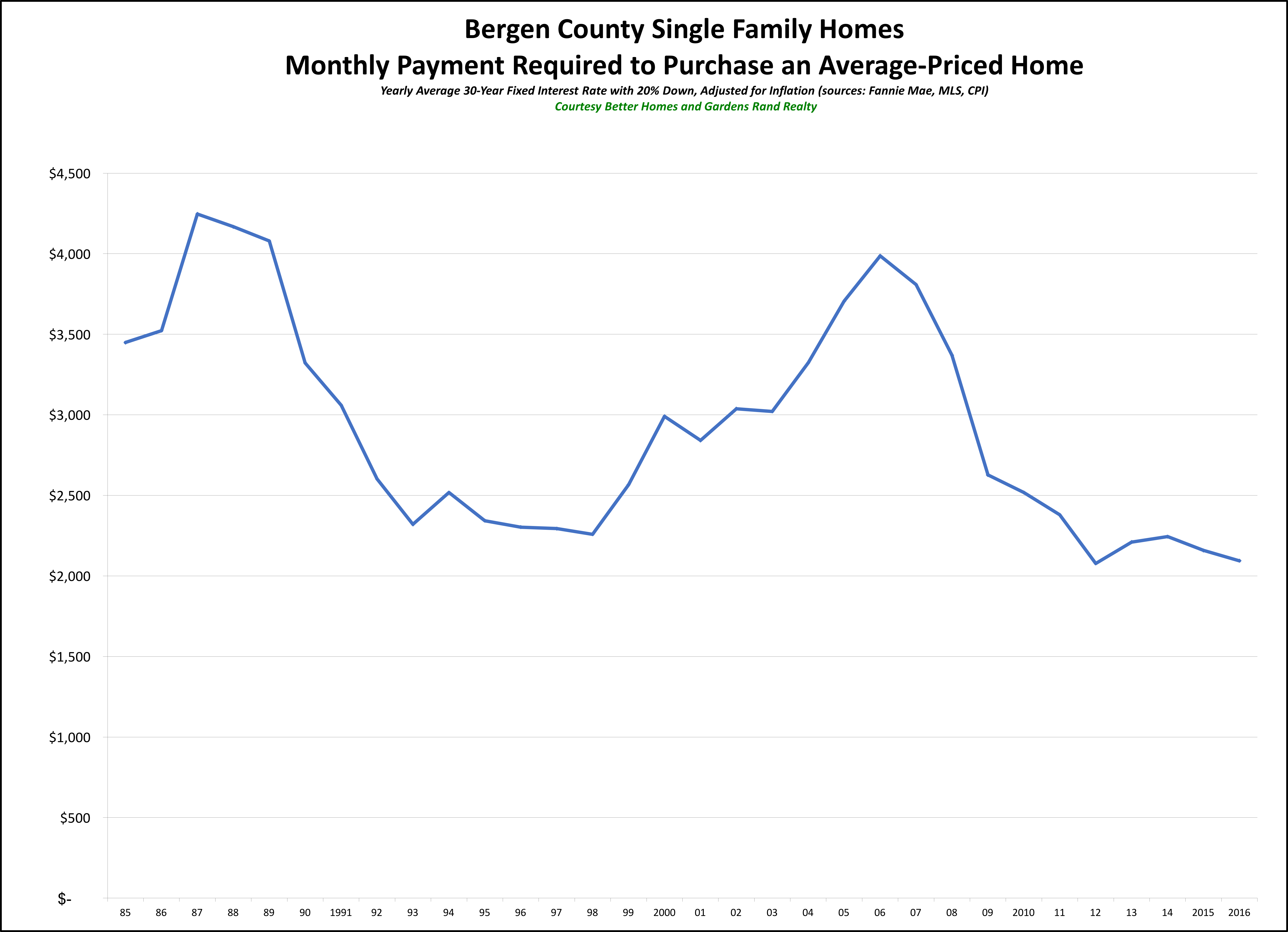

Take a look at these graphs for Bergen and Passaic Counties, and you’ll see what I mean:

On these graphs, as we’ve done before, we’ve plotted the monthly payment that a purchaser in the county would have to make to purchase the average-priced home at various points over the years. After all, affordability is not just a matter of the sales price – it’s a matter of the monthly payment you’re going to have to make, which is partly a function of the prevailing interest rate. And then to measure the change in the monthly payment over time, we factored in the effects of inflation.

So we took the following data points:

•The average price of a single family home up to the end of 2016 – from the local MLS data.

•The average interest rate for a 30-year fixed-rate mortgage for every calendar year up to 2016 – from Freddie Mac.

•The prevailing inflation rate for every calendar year up to 2016– from the US Department of Labor.

You can see the results on the graph. The monthly payment you have to make to purchase the average-priced home in Bergen or Passaic is just about as low as it’s been in years. We saw the slightest uptick from 2012-2014, partially because of a slight increase in pricing and a slow inflating of interest rates. But the payment came down again over the past two years, with rates falling and prices stalling.

Generally, though, we’re talking about a monthly payment that is as low as anytime in the past 30 years – and as low as it was in the mid-1990s, during a crippling buyer’s market. We don’t have data going back in Passaic as far as we do in Bergen, but there’s no reason to think that the markets behaved differently during the 1980s.

So why are monthly payments lower than they’ve been in a generation? A couple of reasons:

1) Prices. Part of it is that we have not seen prices go up in any measurable way in almost 10 years. Home prices peaked in 2006-08, lost about 25-30% of value from 2008-2010, and have bounced around a little since then. But they’re still around 2004 levels — without controlling for inflation.

2) Inflation. Ah, yes, inflation — the value of money goes down a little bit each year as inflation takes a bite. Now, inflation rates have been pretty low over the past 15 years from historical standards, but that little bit each year does add up.

3) Rates. But the biggest reason we’re seeing monthly payments lower than they’ve been in a generation is that rates are still at historic lows. After all, about ten years ago, the average interest rate was about 6%. For the past few years, it’s been below 4%. That’s a huge difference in your monthly payment.

Again, I HATE it when real estate professionals say that “this is a great time to buy,” because at many times in our history that has been bad advice.

But if you measure a “great time to buy” by looking at the monthly payment you’ll have to make to buy a home, then we’re talking about as good a time to buy as any in the past decades. Prices have been flat for almost 10 years, and they’re down significantly if you factor in the effects of inflation. And interest rates are still as low as we’ve ever seen them. Unless we see some major shock to the economy, I think we’re looking at a near-decade of reasonable price appreciation coupled with increasing interest rates – both of which are going to drive that monthly payment up over the next few years.

So I’m not going to tell you what to do. That’s not my job. But if you’ve been thinking about buying a home, I think these graphs speak for themselves.

Joe Rand is the Chief Creative Officer of Better Homes and Gardens Real Estate | Rand Realty, and compiles and writes the Rand Quarterly Market Report.

To learn more about Better Homes and Gardens Real Estate Rand Realty, visit their website and Facebook page, and make sure to “Like” their page. You can also follow them on Twitter.

Homes in Westchester and the Hudson Valley are STILL Cheaper Than They Have Been in a Generation

Right now is a really great time to be buying a home in Westchester or the Hudson Valley.

Man, do I hate saying that. As I’ve explained before, I hate the phrase “great time to buy” for a couple of reasons.

First, people have different needs, and a market that’s great for one person might be terrible for another person.

Second, while markets tend to move together, we do see micro-markets (i.e., towns and villages) that defy larger trends. So while it might be a great time to buy in Village A, it might be not so great in Town B.

Third, and most importantly, though, “it’s a great time to buy!” just seems like a hack thing to say, the kind of thing that TERRIBLE real estate agents have said for generations to get unsuspecting and gullible people to buy an overpriced home. And I think that most people get suspicious when real estate agents talk like that.

So I understand if you’re skeptical. And that’s why I don’t want to just TELL you it’s a great time to buy, I want to SHOW you why it’s a great time to buy.

Specifically, I want to make this specific point: the monthly payment you need to buy an inflation-adjusted average priced home in Westchester and the Hudson Valley is as low as its been in a generation.

Think about what I’m saying for a second. I’m NOT saying that homes are cheaper than they’ve ever been. That’s not true. Depending on the year, homes have appreciated, and if you go back more than 15 years, they’ve appreciated pretty dramatically. I’m just saying that the MONTHLY PAYMENT you need to make to buy the AVERAGE PRICED HOME is lower right now than it’s been in a generation — if you control for the effects of inflation.

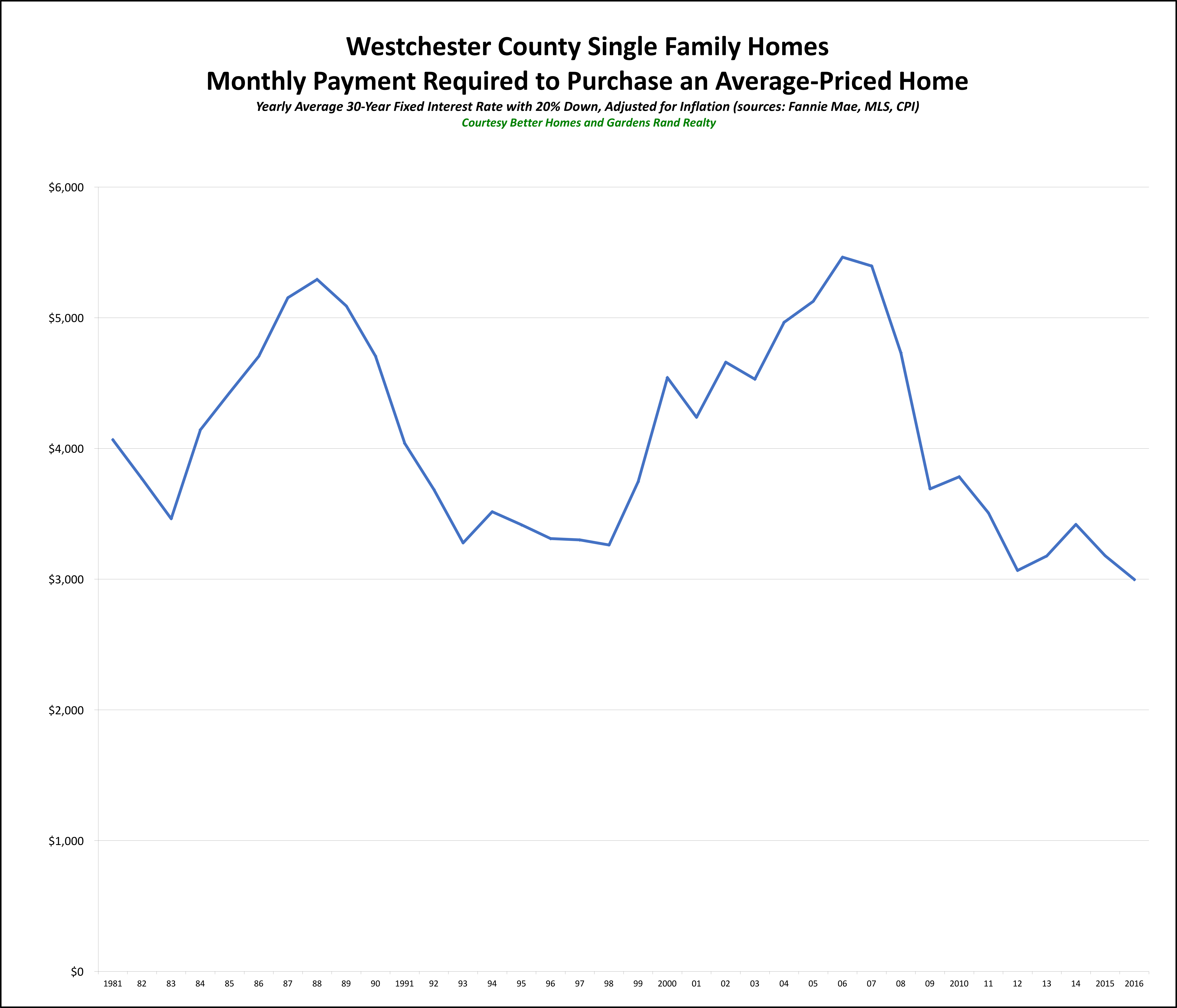

If you look at the graph below for Westchester County, you’ll see what I mean.

On that graph, as we’ve done before, we’ve plotted the monthly payment that a purchaser in the county would have to make to purchase the average-priced home at various points over the years. After all, affordability is not just a matter of the sales price – it’s a matter of the monthly payment you’re going to have to make, which is partly a function of the prevailing interest rate. And then to measure the change in the monthly payment over time, we factored in the effects of inflation.

So we took the following data points:

•The average price of a single family home up to the end of 2016 – from the local MLS data.

•The average interest rate for a 30-year fixed-rate mortgage for every calendar year up to 2016 – from Freddie Mac.

•The prevailing inflation rate for every calendar year up to 2016– from the US Department of Labor.

You can see the results on the graph. The monthly payment you have to make to purchase the average-priced home in Westchester is just about as low as it’s been in years. We saw the slightest uptick from 2012-2014, partially because of a slight increase in pricing and a slow inflating of interest rates. But the payment came down again over the past two years, with rates falling and prices stalling.

Generally, though, we’re talking about a monthly payment that is as low as anytime in the past 35 years – and as low as it was in the mid-1990s, during a crippling buyer’s market.

So why are monthly payments lower than they’ve been in a generation? A couple of reasons:

1) Prices. Part of it is that we have not seen prices go up in any measurable way in almost 10 years. Home prices peaked in 2006-08, lost about 25-30% of value from 2008-2010, and have bounced around a little since then. But they’re still around 2004 levels — without controlling for inflation.

2) Inflation. Ah, yes, inflation — the value of money goes down a little bit each year as inflation takes a bite. Now, inflation rates have been pretty low over the past 15 years from historical standards, but that little bit each year does add up.

3) Rates. But the biggest reason we’re seeing monthly payments lower than they’ve been in a generation is that rates are still at historic lows. After all, about ten years ago, the average interest rate was about 6%. For the past few years, it’s been below 4%. That’s a huge difference in your monthly payment.

And the same is true throughout the Hudson Valley. I showed you Westchester first because we have good data on prices for the county going back all the way to 1981. In other counties, our data doesn’t go back as far, but if we look at each of those counties you can see that it’s pretty much the same story for the time period we have.

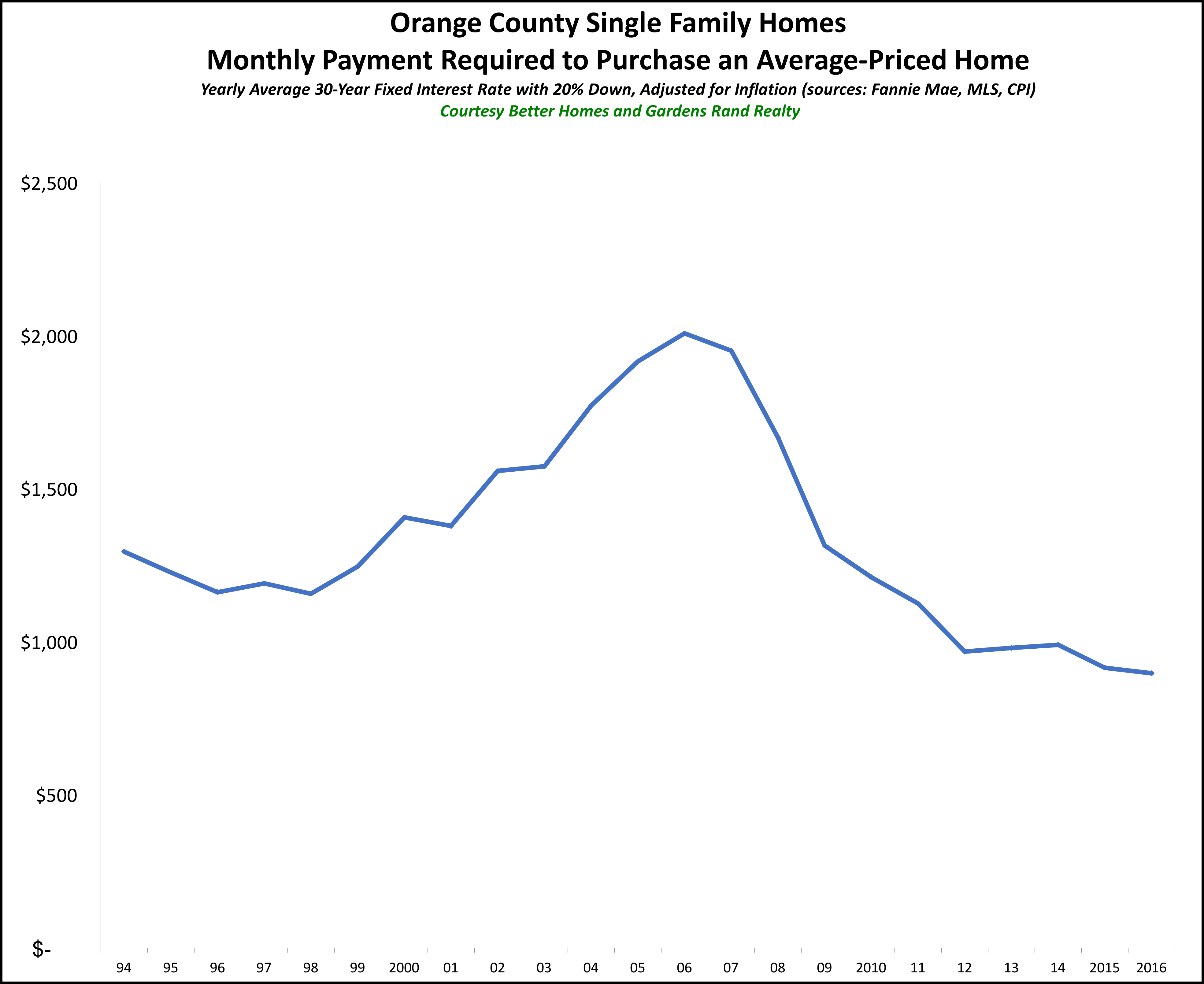

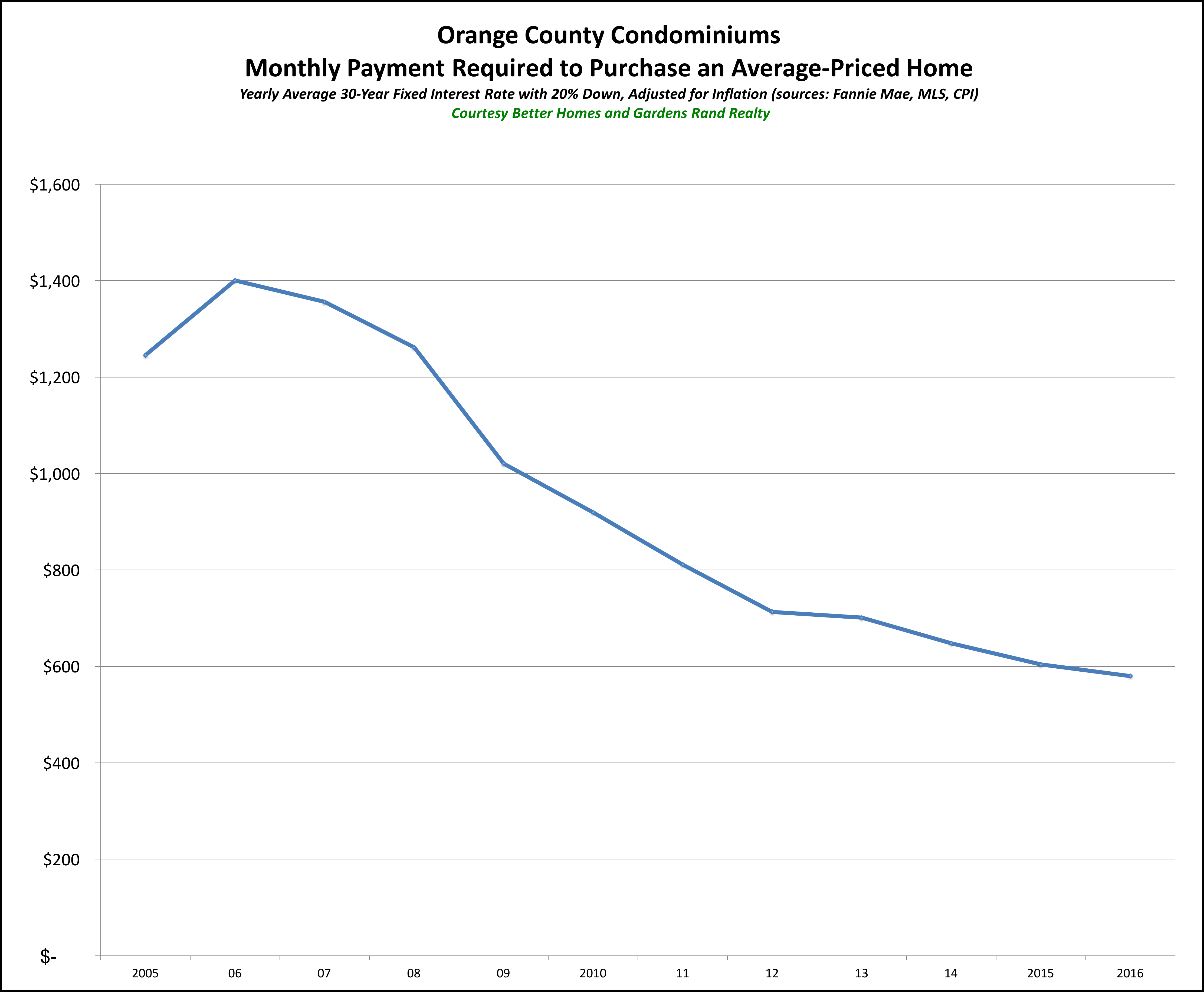

Orange County. Here’s Orange County, where we have data going back to 1994:

You can see that the monthly payment to buy an average-priced home in Orange County is lower right now than it’s been in over 20 years.

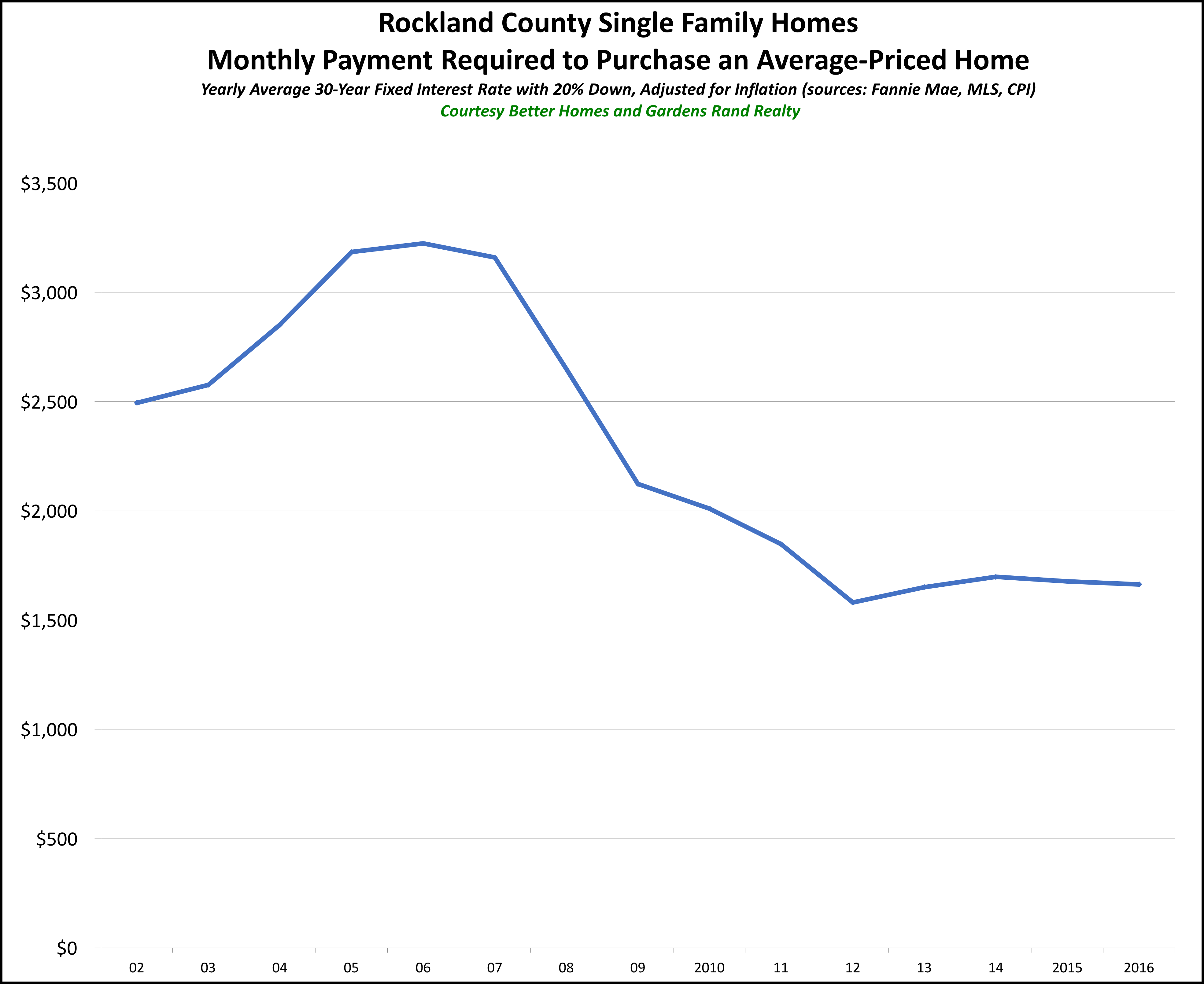

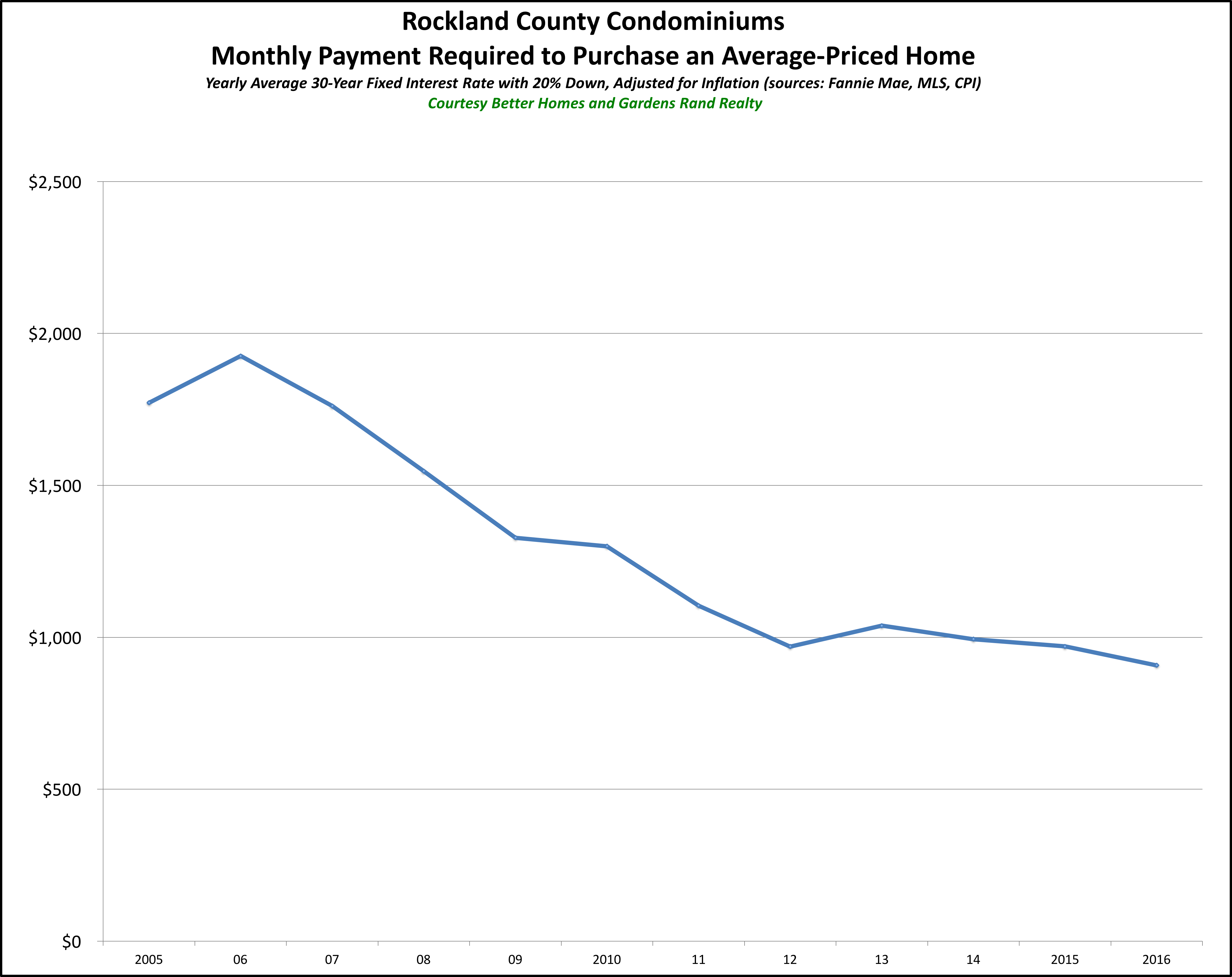

Rockland County. In Rockland, we have data going back to 2002, over 14 years of data.

Again, you can see that even with a slight rise in the past few years, the monthly payment you have to make to buy the average-priced home in Rockland is lower right now than it’s been since at least 2002, and probably for quite a bit of time before that.

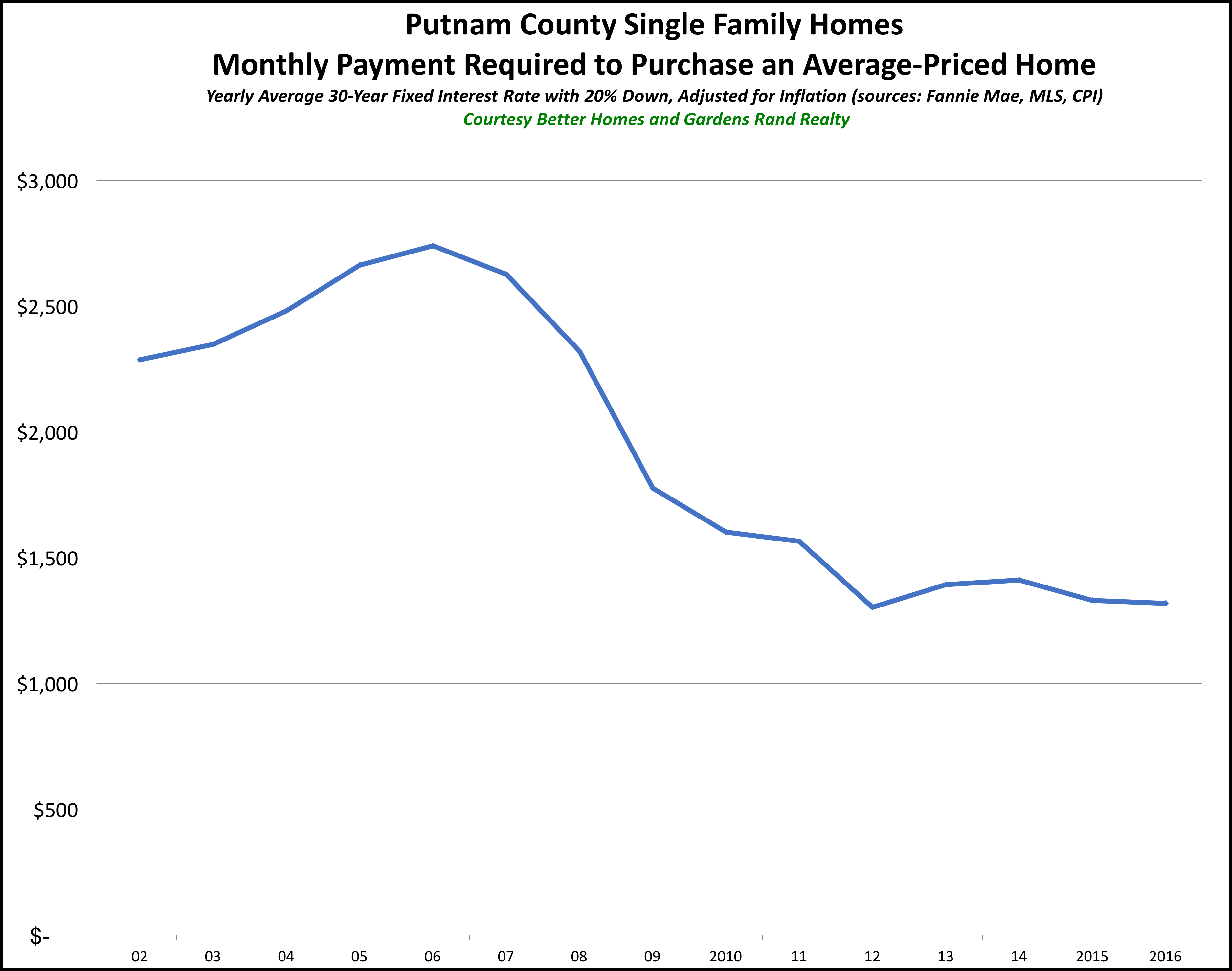

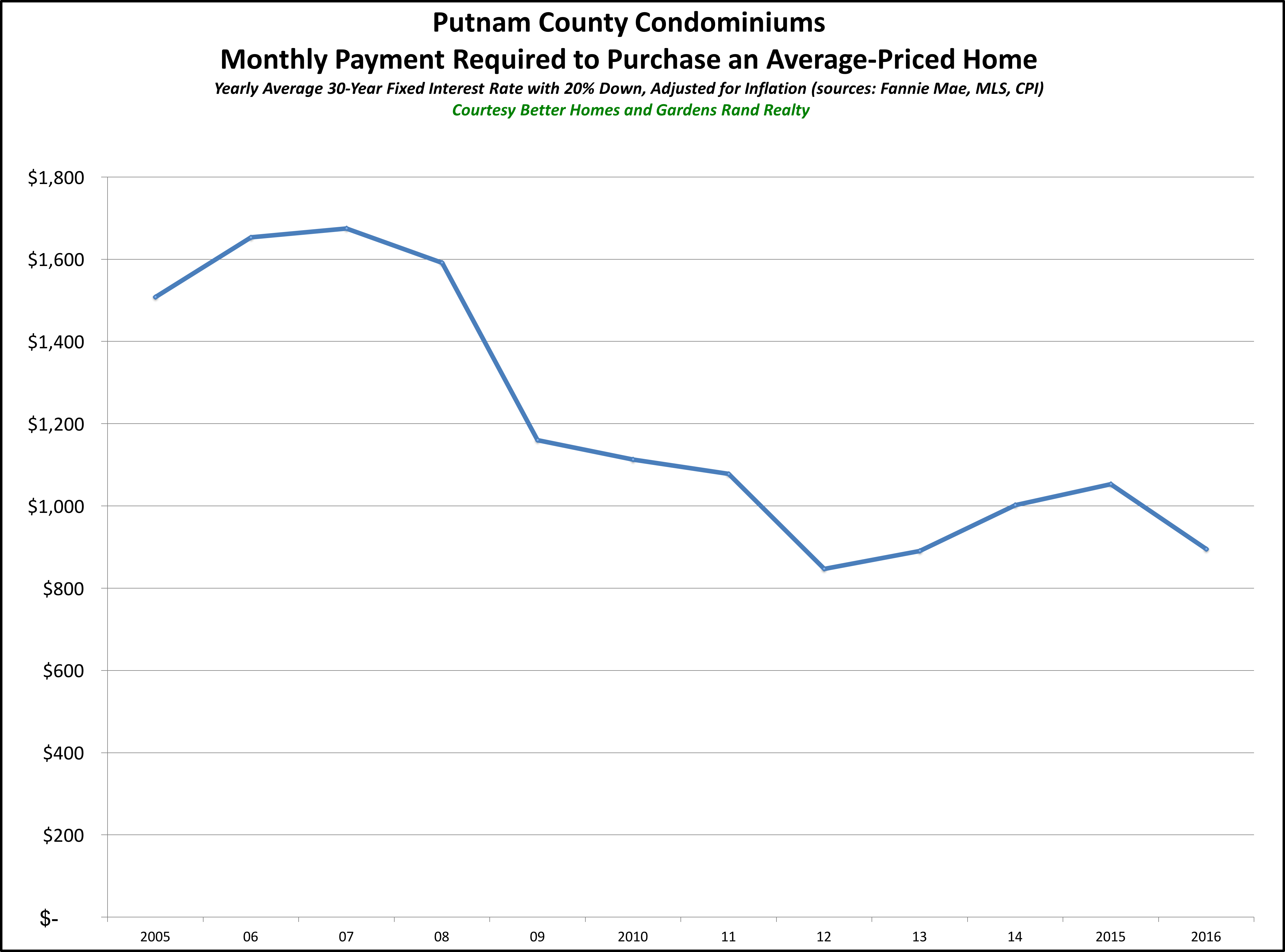

Putnam County. Similarly, we have data going back to 2002 in Putnam, and the story is the same:

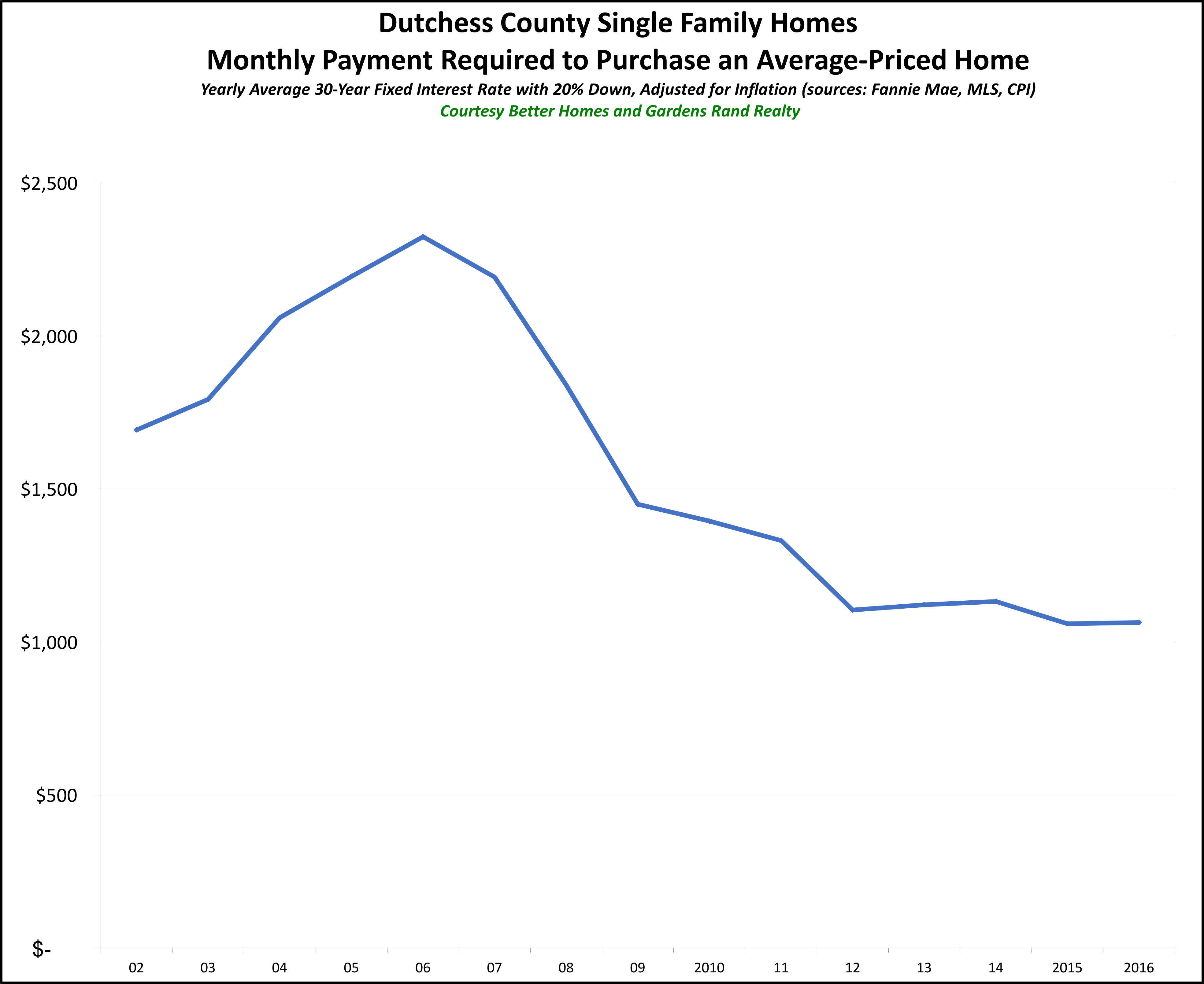

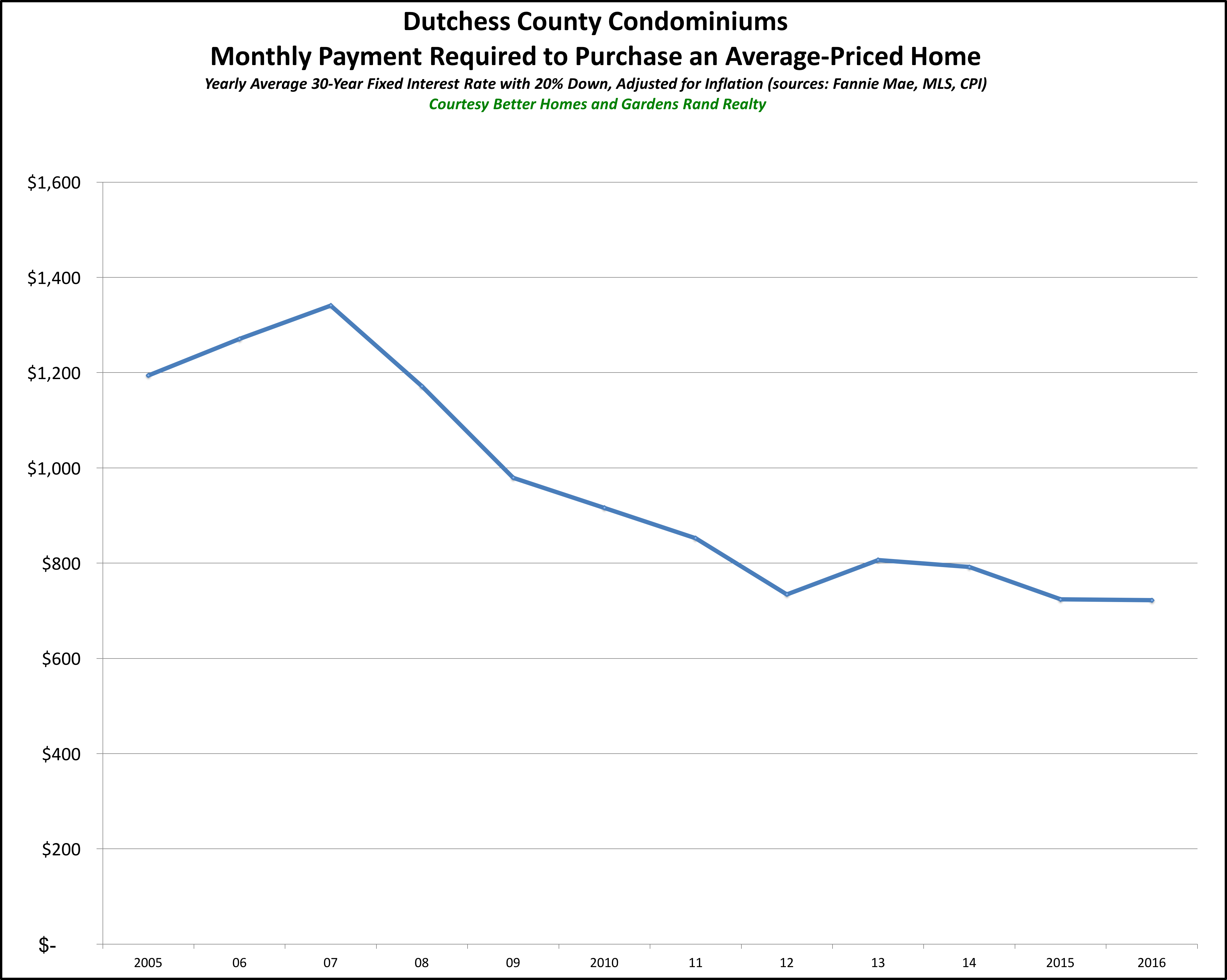

Dutchess County. Again, same story in Dutchess County for that same period:

And although we don’t have data for Orange, Rockland, Putnam, or Dutchess going back as far as Westchester, the fact that the curve over the recent decade or so is very consistent with Westchester’s results suggests that, like in Westchester, the monthly payment you need to make throughout the Hudson Valley is lower right now than it’s been since the Carter administration.

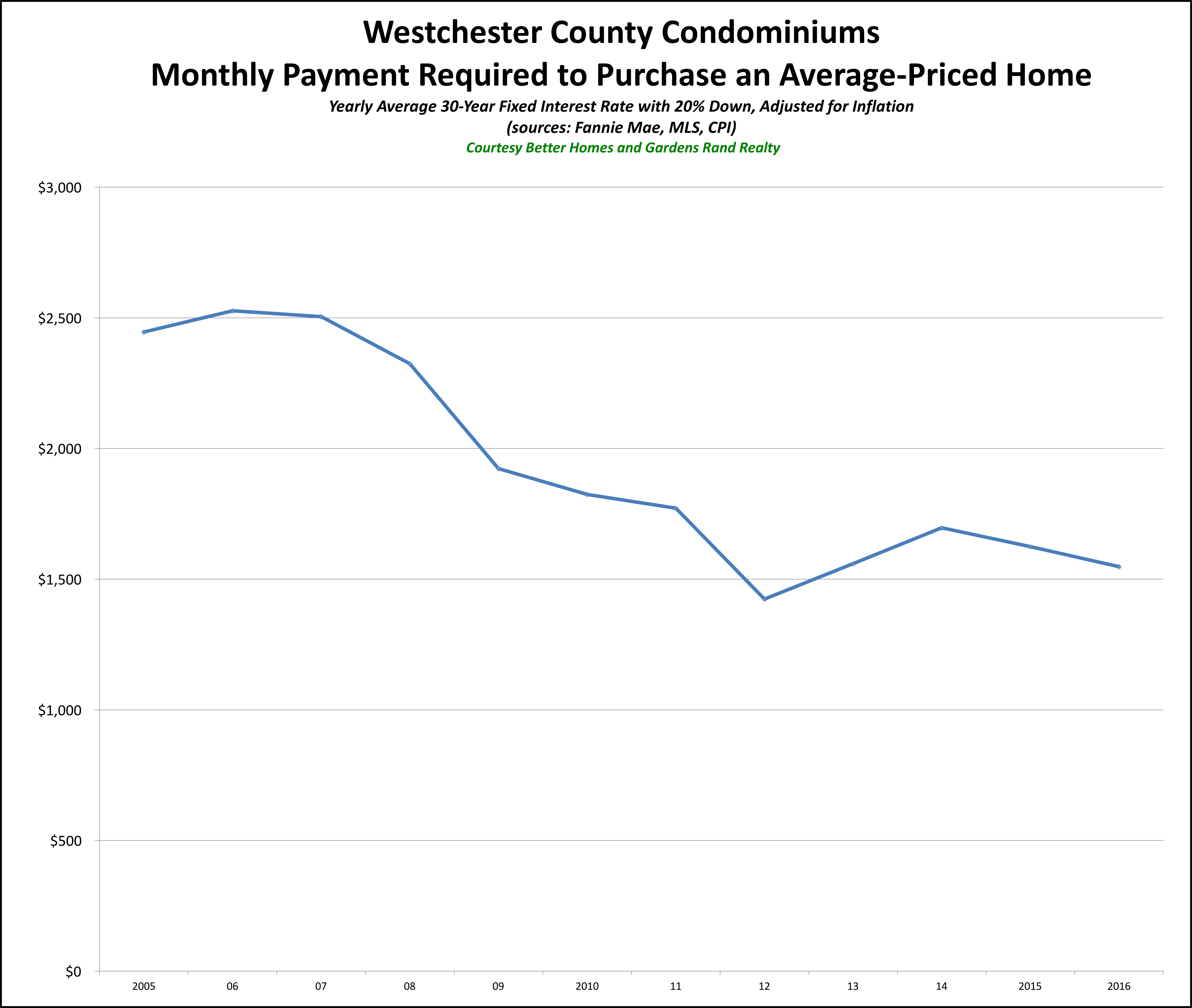

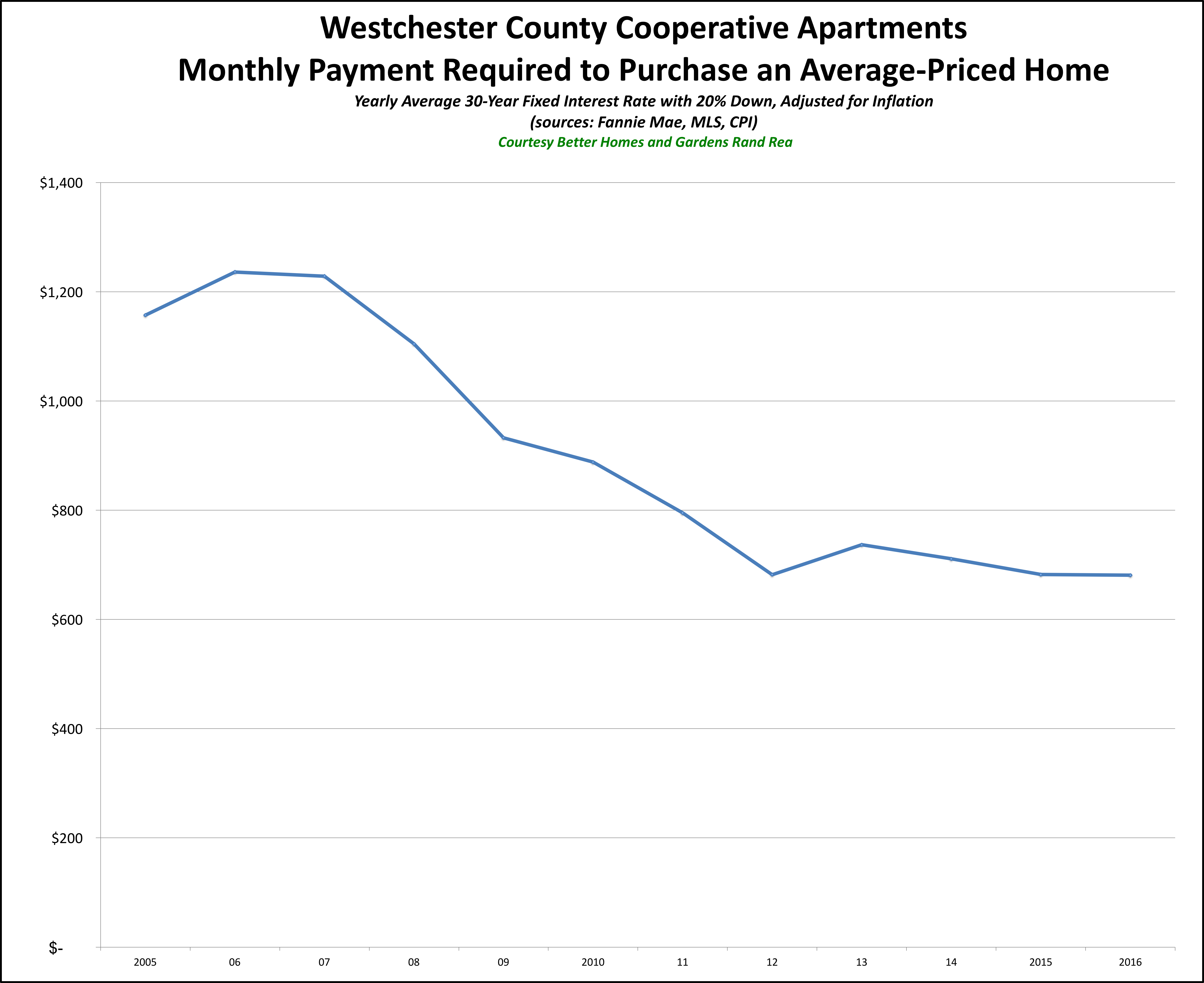

Condos and Coops. All that’s for single-family homes. What about condos and coops? Well, we don’t have data going back as far, but in each county, condos (and coops in Westchester) show the same trend — the monthly payment to buy an average priced condo or coop in the region is lower right now than it’s been at any time since the 2005 era. Here are the graphs:

You can see that except for Westchester and Putnam condos, which have seen some pricing changes in the past two years, the monthly payments are lower than any time since 2005. And even in Westchester and Putnam, they’re lower now than at any time in the last decade, just a little higher than the last two years.

We wrote this up last year, and predicted that 2015 would be the last time we’d be able to say it. Surprisingly, though, prices stayed flat for 2016 while rates stayed down, so we have yet another year where the real monthly payment you have to make to buy the average-priced home in our region is lower than it’s been in years.

Conclusion

Again, I HATE it when real estate professionals say that “this is a great time to buy,” because at many times in our history that has been bad advice.

But if you measure a “great time to buy” by looking at the monthly payment you’ll have to make to buy a home, then we’re talking about as good a time to buy as any in the past decades. Prices have been flat for almost 10 years, and they’re down significantly if you factor in the effects of inflation. And interest rates are still as low as we’ve ever seen them. Unless we see some major shock to the economy, I think we’re looking at a near-decade of reasonable price appreciation coupled with increasing interest rates – both of which are going to drive that monthly payment up over the next few years.

So I’m not going to tell you what to do. That’s not my job. But if you’ve been thinking about buying a home, I think these graphs speak for themselves.

Joe Rand is the Chief Creative Officer of Better Homes and Gardens Real Estate | Rand Realty, and compiles and writes the Rand Quarterly Market Report.

To learn more about Better Homes and Gardens Real Estate Rand Realty, visit their website and Facebook page, and make sure to “Like” their page. You can also follow them on Twitter.

Better Homes and Gardens Rand Realty Quarterly Market Report For 2016Q4 Overall: Westchester and Hudson Valley

Better Homes and Gardens Rand Realty Quarterly Market Report For 2016Q4 Overall: Westchester and Hudson Valley

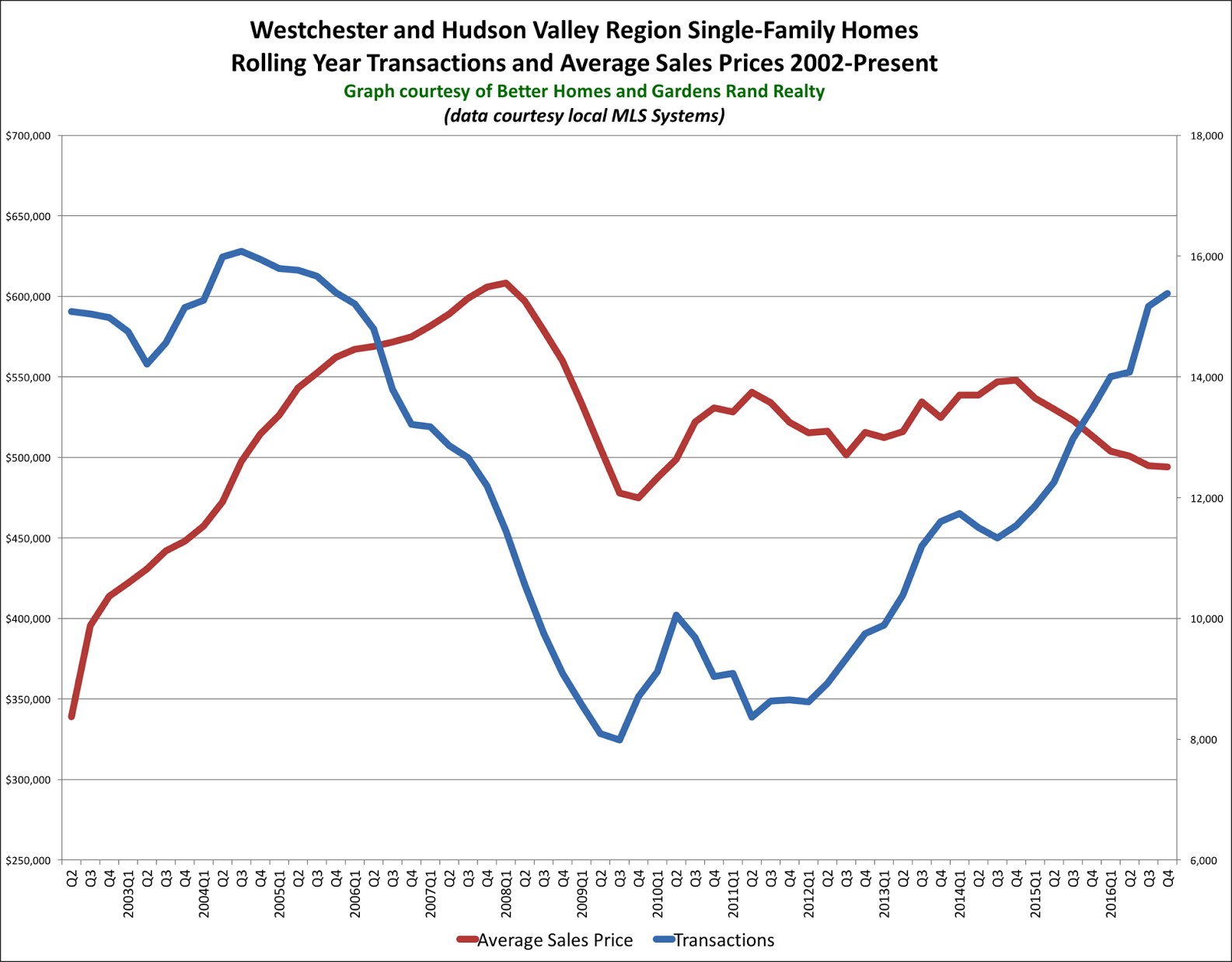

The story of the housing market in Westchester and the Hudson Valley at the end of 2016 was all about inventory. The number of homes on the market continues to decline, which is already negatively impacting the rate of sales growth, but is likely to positively impact price appreciation in 2017.

The story of the housing market in Westchester and the Hudson Valley at the end of 2016 was all about inventory. The number of homes on the market continues to decline, which is already negatively impacting the rate of sales growth, but is likely to positively impact price appreciation in 2017.

Inventory throughout the region continues to fall. As we have explained before in the Rand Report, we measure the “months of inventory” by looking at the number of available homes on the market, and then calculating how long it would take to sell them all at the current rate of absorption. In the industry, we consider anything below six months of inventory to be a signal of a tightening market that will tend to drive prices up. So it’s notable that region inventory at the end of 2016 was down to 6.2 months. But the decline was more striking if you look at the individual counties, with inventory down to 3.8 months in Westchester, 5.0 in Putnam, 4.9 in Rockland, and 6.4 in Orange. Indeed, if you take Dutchess (which is still in the double digits) out of the calculation, the overall regional average is down to 4.2 months of inventory. That’s extraordinarily low, especially when you consider that regional inventory was over 10 months just two years ago.

The lack of inventory is starting to have an impact on sales. Sales are still relatively strong, but the pace of growth is slowing. Single-family transactions were up for the region, rising 6% from the fourth quarter of last year, which now marks nine straight quarters of year-on-year sales growth. And regional sales were up sharply for the calendar year, rising over 14% from 2015 and crossing over the 15,000 transaction mark for the first time since 2005. Indeed, yearly sales are now up 78% from the market bottom in 2011. But we see some troubling signs. For example, that 6% rise in sales from last year is the smallest year-on-year sales increase in eight quarters. Moreover, although regional sales were up, individual counties were flat or down: Westchester was up only 1.4%, and Rockland was down 3.6%. Essentially, the market needs more fuel for the fire — without more listings on the market, we are likely to see sales flatten or even decline in 2017.

Prices continue to struggle throughout the region. The regional average sales price was down just a tick for the quarter, but fell almost 4% for the calendar year. How can that be? We are seeing sustained buyer demand coupled with declining inventory over the past few years, and sales totals that approach the tail end of the last seller’s market. Basic economics tells us that increasing demand and falling supply should drive prices up. And, well, they will. It’s just a matter of time. At some point soon, these high levels of buyer demand, along with the low levels of inventory, will start creating the kind of multiple offer situations and bidding wars that will drive prices up. In turn, as prices go up, homeowners watching and waiting from the sidelines will be tempted into the market, which will moderate the potential surge in price appreciation. In other words, we’re about the witness “Economics 101” in action.

Going forward, we remain confident that the market conditions are ripe for meaningful price appreciation in 2017. Demand is strong, bolstered by near-historically-low interest rates, prices that are still near 2004-05 levels (without controlling for inflation), and a generally strong economy. And supply is tight, at least until some price appreciation brings more sellers into the market. So in the short term, we might see some declines in home sales off the highs set in 2016. But over time, as high-demand-and-short-supply starts driving prices up, inventory will come back. And we will eventually see the return of sales growth, this time coupled with meaningful price appreciation.

To learn more about Better Homes and Gardens Real Estate® – Rand Realty, visit their website and Facebook page, and make sure to “Like” their page. You can also follow them on Twitter.