Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

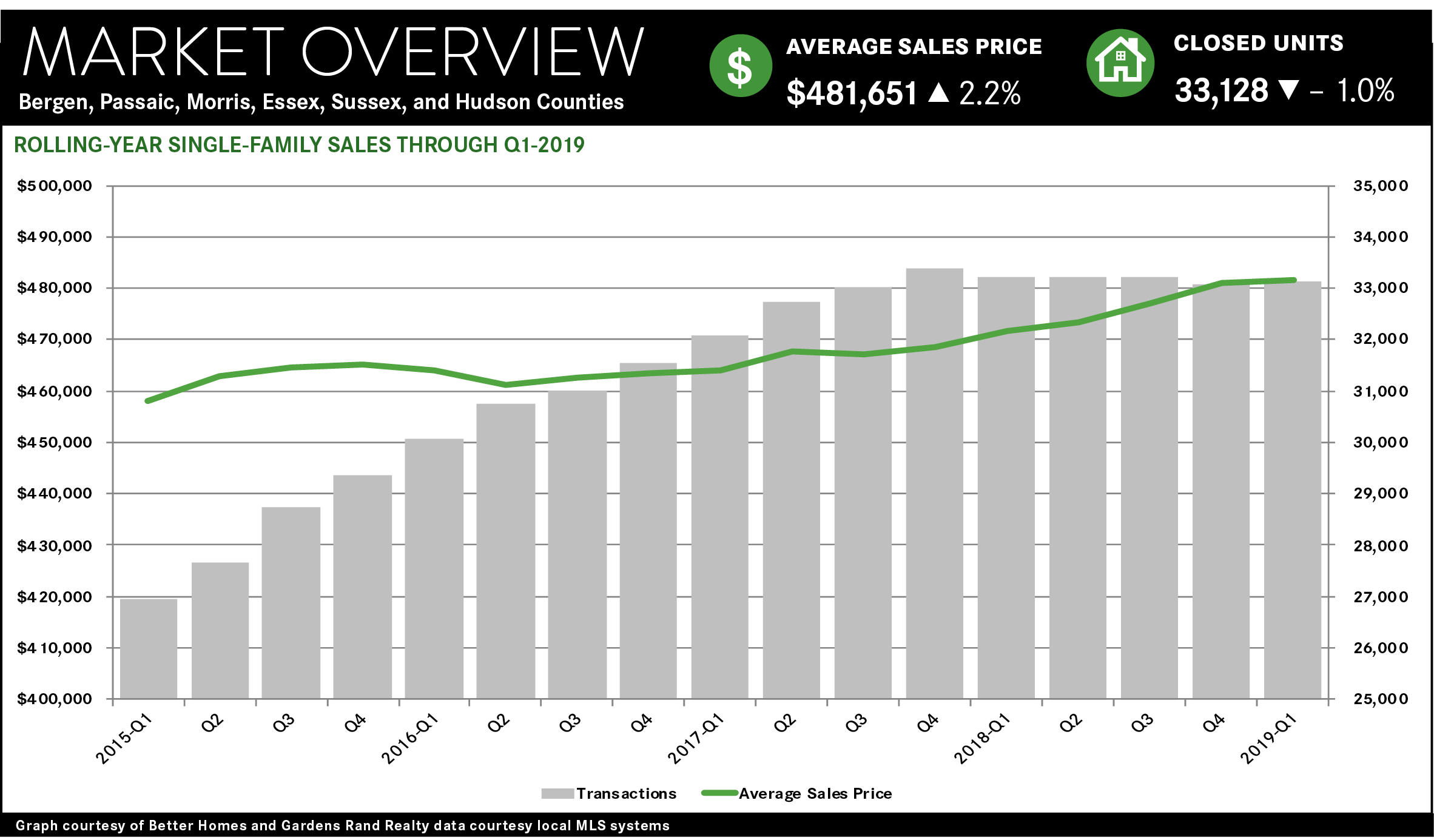

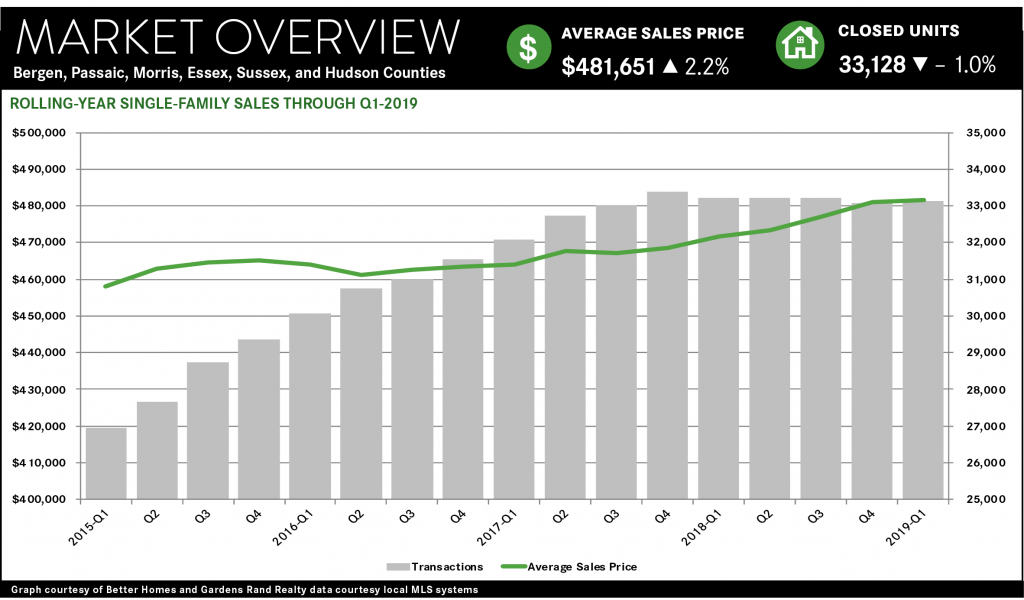

The Northern New Jersey housing market slowed a bit in the first quarter of 2019, with sales down and prices flat. But we believe that the market is still poised for sales growth and price appreciation in what will be a relatively robust spring market.

Regional sales were down, but the results varied by county. Regional single-family sales fell about 4% for the quarter, but that cumulative number masked a real divergence in the county results. For example, sales were down in Hudson, Passaic, Morris, and Sussex, but up in Bergen and Essex. The most significant slowdown was in Hudson, where overall sales fell almost 15% from last year’s first quarter, probably due to the sharp downturn in the neighboring Manhattan market.

Similarly, prices were up a tick regionally, but results were much stronger in lower-priced markets. For the region, the average price was up about 0.5% for the quarter, below the yearlong appreciation of 2.2%. But, again, those cumulative regional results do not really tell the story, since price appreciation varied dramatically by county. For the quarter, the average price fell in all the higher-priced markets—Hudson, Bergen, Morris, and Essex– but rose in the lower-priced counties– Passaic and Sussex. (The results were a little stronger if we look at the rolling year, where every market but Essex saw at least modest price appreciation).

Essentially, we are seeing a “tale of two markets,” with price appreciation higher in lower-priced markets and property types. We believe this divergence has been caused by the 2018 Tax Reform’s cap on state and local tax deductions (“SALT Cap”). When the tax code implemented Tax Reform, we speculated that the SALT Cap might have a more significant impact on higher-end markets. Why? Because taxpayers in those markets are more likely to itemize their taxes and thereby feel the pinch of the $10,000 SALT Cap. But in the lower-priced markets, homeowners and buyers are more likely to be at income levels where they tend to take the standard deduction, meaning that the SALT Cap would have little effect on them.

Essentially, the SALT Cap is suppressing sales and price appreciation in the higher-priced markets like Hudson, Bergen, Morris, and Essex, but having little or no impact on lower-priced markets like Passaic and Sussex. Indeed, we are seeing the same thing throughout the metropolitan region – in the northern suburbs of New York City, for example, prices were down in higher-priced Westchester but up in lower-priced markets like Rockland and Orange. The SALT Cap is not devastating these high-end markets – for example, the rolling year average price in the higher-end counties was still up – but it is hampering what would otherwise be a fairly robust seller’s market.

Going forward, we still believe that the market is poised for growth. At some point, we expect the impact of the SALT Cap to get priced into the market, because the seller market fundamentals are otherwise very strong: the economy is growing, interest rates are near historic lows, inventory is relatively low, and homes are still priced well below their highs. Accordingly, we expect a relatively robust spring market throughout the region.

To learn more about Better Homes and Gardens Real Estate Rand Realty, visit their website and Facebook page, and make sure to “Like” their page. You can also follow them on Twitter, Pinterest, and Instagram.