Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Qualities of a Great Agent

The most common question asked by people considering a career in real estate is, “What are the qualities of a great real estate agent?” (Okay, maybe that’s the second question after “How much money can I make?”)

Let’s look at the typical qualities of top-producing real estate agents:

- Hard working

- Goal-oriented

- Persevering

- Technologically proficient

- Self-motivated

- Ambitious

- People-oriented

- Flexible

- Attentive

- Willing to learn

- Service-oriented

- Confident

- Communicative

- Organized

The one common denominator that all successful agents share regardless of age, background, or previous experience is attitude. Successful agents have an attitude of success. The right frame of mind allows them to overcome any obstacle in order to meet their objectives with dignity, grace, and professionalism, while having fun and enjoying life at the same time!

As for the money question, the rewards of a real estate career do include a potential for high earnings. Your income directly reflects your efforts but successful agents will tell you that status in the community, autonomy, flexible schedule, helping people, the intellectual challenge, and the satisfaction from those accomplishments are equal to or greater than the financial rewards.

Do some research on becoming an agent now by trying our Real Estate Simulator, where you can:

- Play the role of an agent.

- Interact with virtual clients interested in buying or selling property.

- See how you measure up to the top performers in the industry.

What to Expect

Prospecting is the single most crucial element in the business and presents the biggest challenge for most real estate agents.

Prospecting can be done in a number of ways:

- Contacting your sphere of influence

- Open houses

- Office inquiries

- Online techniques

- Canvassing

- Handing out business cards

- And lots more!

The important thing to realize is that it’s not easy, but must be done consistently in order to have a successful real estate career.

Some other activities you could expect to do on a daily basis:

- Tour new listings

- Preview homes

- Staying updated on real estate-related laws and issues

- Conduct and attend open houses

- Spend ”floor time” at the office

- Attend closings with your clients

- Maintain relationships with your sphere of influence

- Follow up with clients and customers

- Prepare contracts for purchase and presenting offers for buyers, and offers from others to your sellers

- Complete market evaluations

- Show homes to prospective buyers

- Prepare and present listing proposals and marketing plans

- Facilitate communication between all the parties involved in the transaction

Do some research on becoming an agent now by trying our Real Estate Simulator, where you can:

- Play the role of an agent.

- Interact with virtual clients interested in buying or selling property.

- See how you measure up to the top performers in the industry.

NY Tax Grievances: Frequently Asked Questions

As part of putting together this Guide to Grieving Your Property Taxes, we anticipated a number of questions that you might have about the process. So we’ve gathered them together into this list of “Frequently Asked Questions” and our answers.

Q: Do I need to hire an attorney to represent me?

You do not need to hire an attorney, but it helps. We have provided information in our Guide to Grieving Your Property Taxes about how to file your own grievance. All you really need is to do some research on why you think you are over-assessed, fill out a form, write a letter, and maybe attend the hearing. That said, we actually do recommend you get an attorney, because (1) if you are not successful, you will likely want to appeal, something that really should be done by an attorney, (2) preparing your grievance papers can take a bit of time that you might not have, and (3) attorneys do not charge you unless you are successful. Most attorneys charge a percentage of your first year’s savings, without any upfront fees or filing fees unless you need to appeal the determination. It’s a good deal, and worth it to make sure you get the best representation possible. If you need an attorney, just let us know and we’ll refer you to an experienced professional who can handle your case.

Q: Can I get help from my Better Homes and Gardens Rand Realty agent?

If you are currently listed with Better Homes and Gardens Rand Realty, or if you’ve purchased a home with us, we can help you do the research on comparable sales to determine whether you are over-assessed. Key to your grievance is proving that the assessor’s determination of your market value is too high, and you need access to recent sales data to support this. We are happy to help with that effort. If you do not have a Better Homes and Gardens Rand Realty agent, just contact us at 845-825-8047 and we will put you in touch with someone who can help.

Q: When I file a grievance, what am I really challenging: the taxes or the assessment?

When you file a grievance, you are simply challenging the Assessor’s calculation of the market value of your property. You are not challenging the amount of the property taxes that you will pay. Rather, if you are successful getting a re-assessment of the market value, the reduction in market value will thereby reduce your assessed value. And because your property taxes are based on your assessment, the reduction in the assessment will ultimately lower your taxes. You won’t know your actual property tax amount until a few months after Grievance Day.

Q: Do I need to grieve my village and town tax separately?

Although you likely pay property tax assigned to multiple municipalities and your school tax, all those taxes are based on the assessment. Reducing the assessment will reduce all the types of property taxes you pay. You don’t need to challenge each property tax authority separately, although in many villages in Westchester and the Hudson Valley the village has its own assessor and its own grievance schedule. In those villages, most of which have a February deadline for grievances, you need to grieve the assessment by both the town and the village. You can get a list of all villages that have their own assessment schedule at the end to this Guide.

Q: Do I have to grieve my taxes, or will the Assessor reconsider my assessment?

Most municipalities allow for an informal “review” of your assessment with the Assessor, where you can present your case without having to file a formal grievance. In some cases where you are clearly over-assessed, the Assessor might agree to reconsider the determination of your market value and enter into a stipulation with you for your assessment. The requirements for requesting an informal review vary by municipality, so check the end of this Guide for information about how to request a review with the Assessor. At the very least, there is no harm in calling up the Assessor’s office and asking for the review. The worst that can happen is that they turn you down, and you’ll then file your grievance.

Q: What proof do I need to challenge my assessment?

You just need evidence that your home is worth less than the Assessor’s valuation. This could take the form of an assessment, your recent sales price (if you recently purchased the home), or your listing price (if you are on the market). You can also provide evidence of what other homes have sold for, which you can get in a “Simple CMA” from your Better Homes and Gardens Rand Realty Agent.

Q: Do I need to hire an appraiser to challenge my assessment?

For a grievance, you do not need to pay for an appraisal. You can establish market value by using comparable sales for the past year or so. If you do have an appraisal, which you would have gotten if you refinanced or purchased your property recently, the appraisal will help establish market value and you can include it in your petition. And you might need an appraisal for an appeal if your grievance is unsuccessful. But you do not need it for the grievance.

Q: Can I file a grievance if I previously filed one?

The rule is that you cannot file a grievance only if you filed a successful one in the previous year. If you did not file a grievance last year, you can file this year. If you filed last year and were not successful, you can file this year. But if you filed last year and were successful in reducing your assessment, you cannot file this year.

Q: If I lose, will the municipality actually raise my taxes?

Grieving your taxes is a no-lose situation. Once the assessor establishes a market value, the municipality will not raise it just because you challenged it and opened the issue. We have never heard of a situation where the municipality actually raised the assessment as a result of the grievance, and believe that any municipality trying to do so would risk a lawsuit for retaliation or free speech violations. You get a free bite at the apple.

Q: Do I have to attend the Grievance Day hearing?

You don’t have to attend, but it helps. Once you file your grievance petition with the municipality by the deadline, your petition will be included on the list of grievances for Grievance Day. On Grievance Day, the municipality holds hearings on all the petitions. You have a right to be present at the hearing to present your case, but you don’t actually have to attend. It’s a good idea, though, if you feel that you could articulate your case and persuade the panel.

Q: What if I miss my municipality’s deadline for filing the grievance?

The deadlines for filing a grievance are hard deadlines. If you don’t get your grievance in by Grievance Day, you’ve missed your chance for the year and will not be able to grieve your taxes. For most municipalities in the area, the window is between the first week of May, when the roll is published, and the last week of May, which is grievance day. In most areas of Westchester, Grievance Day is in June. You can check the end of this Guide for a list of municipalities and their deadlines.

Q: If I am successful, am I hurting my municipality or my schools?

Some people get concerned that grieving their taxes might strip their local municipalities of revenue needed to fund schools and other services. But that’s not how grievances work. If you’re successful, you will reduce your own taxes, but not at the expense of revenue needed by your municipality. Rather, the municipality determines how much revenue it needs and sets a tax rate that is applied to all property owners. Your grievance will simply reduce your share of that burden. While it does mean that your burden will be shifted to other property owners, that’s only because you were over-assessed in the first place and paying more than your fair share.

Back to Main Tax Grievance Guide

Understanding the New York Tax Grievance Process

Most people think that the property tax grievance process is complicated. It’s not. It only requires you to do a bit of research, fill out a form, and write a supporting letter, and get all your paperwork submitted by your municipality’s deadline. Here is a brief (and somewhat simplified) overview of that process.

The Assessment

People sometimes think that their property taxes are set by their assessor. That’s not the case. Your municipality’s assessor does not determine your property taxes. Rather, the assessor’s role is only to determine what the market value is for your property by performing what is essentially the same sort of comparable sales analysis that a real estate agent or appraiser conducts when determining the value of your home when you are buying or selling.

Once the assessor has determined your market value, the assessor then calculates your assessed value, which is a simple mathematical calculation that multiples the market value by a predetermined Uniform Percentage of Value set by the state. The purpose of the Uniform Percentage of Value (“UPV”) is to provide a standardized assessment calculation to ensure that every property receives an equitable assessment. So, for example, if the UPV is 40%, and your market value is $500,000, your assessed value would be $200,000 ($500,000 times 40%). If your neighbor’s home has a market value of $400,000, her assessed value would be $160,000 ($400,000 times 40%).

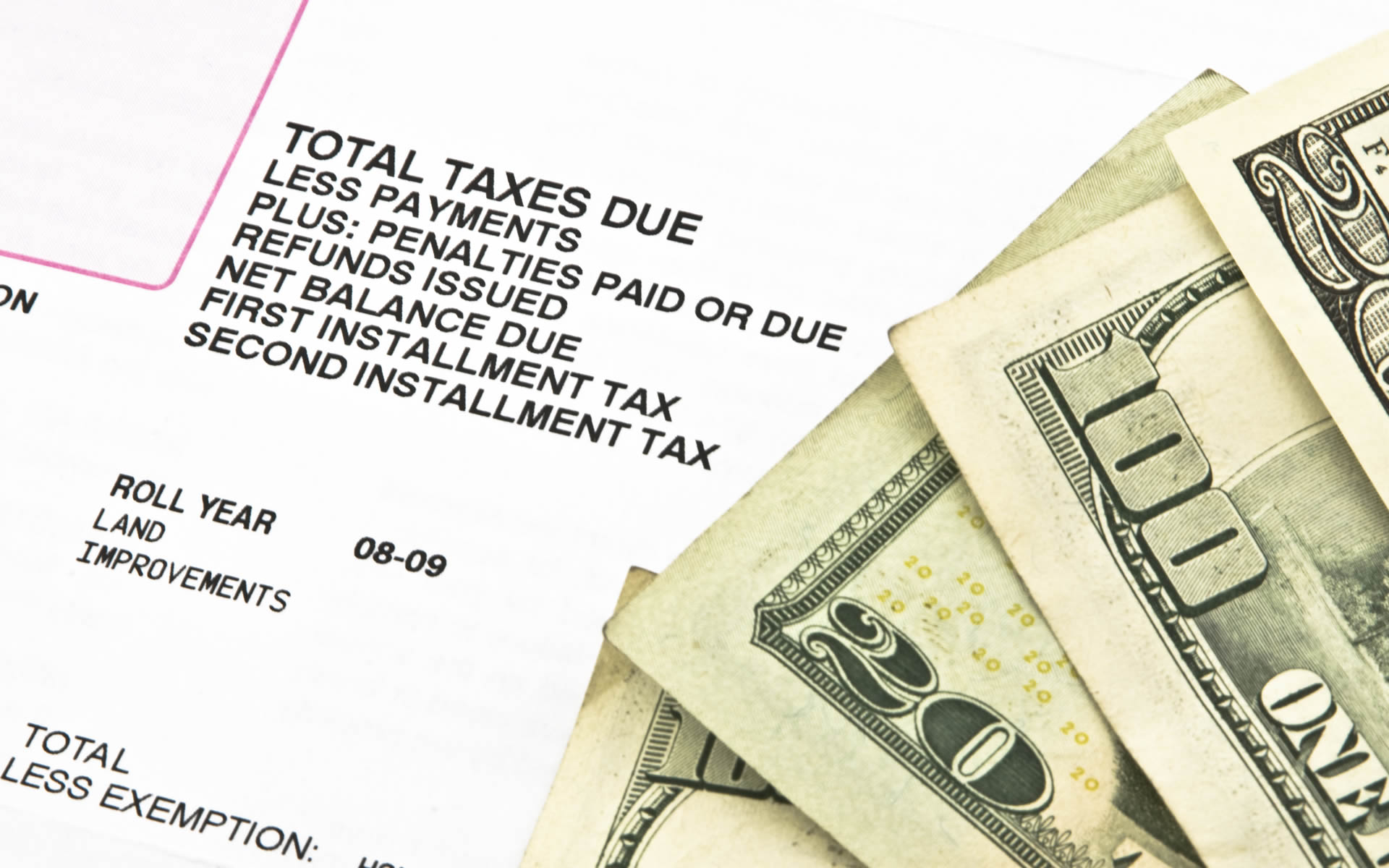

The Assessment Roll

Once the assessor has determined the assessed value of all the properties in a municipality, the assessor’s office will publish what’s called the “roll,” which is a comprehensive listing of all properties, their determined market value, and their assessed value. For most municipalities, the roll is published in the first week of May, a few weeks before grievance applications are due. You can get the roll by going to your local municipality, and in some cases online. You can check on www.randrealty.com after May 1 for links to your local roll publication.

The purpose of the roll is to provide property owners with fair notice to prepare their grievances once they see the assessor’s determination of their market and assessed value. Again, the roll does not state your property taxes, but provides the market value and assessed value upon which your taxes will be based.

Researching Grounds for a Grievance

Once you know the market value determined by the assessor, you can decide whether you have grounds for filing a complaint about your assessment. Technically, property owners can make four distinct claims for a grievance, including situations where the property is improperly classified (i.e., it’s not commercial property, it’s residential) or exempt from taxation (i.e., it’s a church or school). But the main grievance situation for most homeowners involves the basic complaint that the property is subject to an “Unequal Assessment” because owners of comparable properties have received lower assessments and thus will pay lower taxes.

Essentially, a claim of “Unequal Assessment” boils down to this: you contend that the assessor over-estimated the market value of your property, leading to an inflated assessment value, resulting in your having a higher assessment than other owners of comparable properties. In order to prove that claim, you need to show that the market value of your property is actually lower than the assessor’s determination.

If your review of your property’s market value demonstrates that the assessor’s determination of your market value was too high, then you have solid grounds for filing a grievance petition.

Grievance Day

You have to file a complaint grieving your property taxes by the deadline established by your municipality. The deadline is usually a few weeks after the roll is published, and is called “Grievance Day” in most of the Hudson Valley (Westchester has a “Grievance Period” that runs about three weeks, and ends with the deadline day that we’ll call the “Grievance Day.” On that day, a Board of Assessment Review (“BAR”) will meet to start the process of evaluating all the grievance petitions, and will hold an open hearing in which you can present your case.

You only need to submit two documents to file a petition to grieve your property taxes. First, you need the Complaint on Real Property Assessment for (Form RP-524), which is a standard New York State form used to file grievances across the state. The form mostly requires you to fill out information on you, your property, and the nature of your grievance.

Second, you need a letter in support. The state does not particularly stipulate what the letter should look like or contain, or mandate that the letter be typed, but for best results we suggest typing up a simple letter addressed to the Board of Assessment Review for your municipality, including a brief explanation of why you believe that you are over-assessed. As part of that letter, you can attach any documents that support your case, including an appraisal, comparative market analysis from your real estate agent, public records, or anything else that would substantiate your claims.

In your petition, you should ask for the specific relief you want – a reduction in the market value to the lowest level that you think is justified. You should always ask for as much relief as you believe you can possibly get.

You can attend the Grievance Day hearing if you wish to state your case, but even if you do not appear the BAR will consider the petition and make a decision within a short time of Grievance Day.

Appeals

If your grievance complaint is not successful, are not successful, or you get relief but not as much as you asked for, you can appeal the decision in what’s called a Small Claims Assessment Review (SCAR) or a Supreme Court trial. We are not going to cover the details or requirements for that review here, but you can get information provided by the State in the What to Do if You Disagree with Your Assessment booklet that is available online (the link is below).

Conclusion

Grieving your taxes is easier than you think. You simply need to pay attention to what’s happening in the local community, review the assessment roll, and get your complaint and supporting documents submitted by Grievance Day. That said, if you don’t want to do it yourself, you should consider hiring an attorney to represent you. Attorneys who handle tax grievances generally charge between 40-50% of the first year’s savings on your taxes, so they only charge you a fee if they are successful. And you will likely need an attorney anyway if you are not successful and choose to appeal the BAR decision.

If you would like some additional information, the State of New York has prepared some materials that you might find helpful:

What to Do if You Disagree with Your Assessment

http://www.orps.state.ny.us/pamphlet/complain/howtofile/whattodo.pdf

A guide from the State of New York for property tax grievances and appeals.

Complaint of Real Property Assessment for (RP-524)

http://www.orps.state.ny.us/ref/forms/pdf/rp524.pdf

The actual form you need to file a tax grievance.

General Instructions for Filing Complaints on Real Property Assessments (RP-524-Ins)

http://www.orps.state.ny.us/ref/forms/pdf/rp524ins.pdf

Instructions for filling out the tax grievance complaint form.

Thank you for taking the time to read this. Good luck in your property tax grievance. If you need anything from Better Homes and Gardens Rand Realty, just call us at 845-825-8047.

Back to Main Tax Grievance Guide

Introduction to Tax Grievances in NY

TO OUR CLIENTS:

At Rand Realty, we believe that service to our clients does not end just because you have closed on the purchase or sale of your home. Rather, most client need professional real estate services all the time, everything from keeping up-to-date on market news, changes in property values, or information on their local communities. That’s why, for example, we’ve put out Quarterly Market Reports and Seasonal Event Guides for our clients for over ten years.

In that spirit, we created The Guide to Grieving Your Property Taxes in Westchester and the Hudson Valley to provide you with a simple but comprehensive guide to challenging your property tax assessments. While we understand that our local communities need revenue to fund the schools and services that make our communities such desirable places to live, we also believe that property taxes should be fairly apportioned among property owners. In our experience, though, too many homeowners pay more than their fair share of property taxes because assessors have over-estimated their market value, and those high property taxes can become a tremendous financial burden. And for our current clients who are selling their homes, unreasonably high property taxes can become a challenge for selling at a fair price.

As this Guide explains, challenging your assessment and grieving your taxes is a complicated but manageable process. We are happy to help you in that effort, particularly by providing you with information on comparable sales that can help you determine your market value and support a case for lowering your assessment. We are also happy to help you if you would like an attorney to assist you in filing your grievance, which we believe is a good idea because of the difficulties of the process and also because most attorneys only collect a fee based on your savings if you are successful.

Here is what we have in the Guide:

- Understanding the Property Tax Grievance Process: An explanation and overview of the entire process.

- The Property Tax Grievance FAQ: Common questions and answers about the grievance process.

- Three Steps to Grieving Your Taxes: Step-by-step instructions for determining market value, filling out your complaint, and writing your letter in support.

- Five Reasons to Hire an Attorney to Represent You: An explanation why we recommend that you retain an attorney to represent you through the grievance process.

- Grievance Day Deadline Summary: A review of all the deadlines for filing your tax grievance throughout Westchester and the Hudson Valley.

Under separate cover, you can also get the Better Homes and Gardens Rand Realty Property Tax Grievance Municipality Guide, which contains detailed information on each municipality, including contact information, tax grievance deadlines, and more.

If you would like our help providing you with market information on comparable sales that can help you challenge your assessment, or if you would like us to connect you with an experienced grievance attorney, just contact your Rand Realty agent. If you do not have an agent, then just contact us at 845-825-8047 and we’ll take good care of you.

Good luck, and best wishes.

Yours,

The Rand Family

Back to Main Tax Grievance Guide

Download the Complete Tax Grievance Guide

How to Resolve Disputes with Your Landlord

Hopefully, your tenancy will be uneventful. You’ll enjoy living in the property, you’ll stay through your full term, and you’ll move out when the lease is over. But what happens when you want to get out early, stay late, or not live there at all? Here is a guide to resolving common disputes with your landlord.

In some cases, tenants end up in unavoidable disputes with the landlord. It might not be the fault of either party, but you might have a situation where you want to move out early, stay in the tenancy longer than your term, or move out because of livability issues in the property.

When you have an issue with your landlord, try to resolve it amicably and collegially. You don’t need to immediately start a fight with your landlord, or assume that the landlord is acting in bad faith. Generally, you always want to have good relations with your landlord, so the landlord can act as a reference for your next tenancy. You also, if possible, want to be able to recover your security deposit, which becomes more difficult if you generate animosity with your landlord. Most issues can be resolved fairly, even difficult ones, if both parties work in good faith. Your landlord does not want a fight any more than you do.

Here are some major issues that come up in tenancies, and how to deal with them.

Livability Issues

Every residential lease carries with it an implied right for tenants to live in a “habitable” property. This means that the property has to have structural integrity, have a lock, and be free of defects such as smells, vermin, or continual loud noises that might make it impossible to live in. Even if those defects are not technically the landlord’s fault, the landlord has an obligation to provide you with a livable property in order to collect your rent.

This “implied warranty of habitability” is legally imputed to every lease, so it does not need to be spelled out, but it generally applies to serious defects, not minor annoyances. A roach problem that can be resolved with an extermination or over-the-counter bug spray does not rise to the level of a breach of the landlord’s duty to provide a livable space.

If you do have problems with the condition of the space, it’s a good idea to send a letter (or an email) to the landlord spelling out the problem and asking for help. Your communication should not be aggressive or accusatory. Rather, simply point out the problem, and ask for the landlord’s help in resolving it. Most landlords are open to fixing these types of problems to maintain good relations with tenants. Trust that your landlord will act in good faith when you make your request for assistance.

If that does not resolve the problem, and if the property is truly uninhabitable, that can give rise to your right to terminate the lease without further obligation. If you think it’s serious enough to force you to consider breaking the lease, you can then take more aggressive action by sending a formal written letter to the landlord spelling out the problem and demanding resolution. In the letter, state that if the problem is not resolved in a reasonable time, you will be forced to vacate the property for breach of the implied warranty of habitability. Hopefully, this will get the landlord to act.

If you need help resolving these issues, approach the agent who helped you lease the property, who will have experience handling these problems and might be able to assist you. Landlords want good relationships with real estate agents and brokers, so an agent stepping in to help you negotiate a resolution to the problem might compel the landlord to take you more seriously.

Breaking Your Lease

Sometimes, tenants want to break their lease before the end of their term for personal reasons. Maybe they got transferred, or fell in love and want to move in with their new significant other, or they lost their job and cannot afford the rent anymore. In these cases, it is paramount that you approach your landlord with honesty, because you essentially are asking the landlord to do you a favor.

In these cases, the best thing to do is approach the landlord as soon as possible, explain the situation honestly, and ask to be released from your lease obligations. In fairness, you should be willing to cover the rent obligations until the landlord is able to find a replacement tenant, or at the very least for the rest of the current month and one month longer. You should also be willing to forego the security deposit if the landlord is not able to find a replacement tenant within several months of your early termination.

In most cases, the landlord going to be amenable to your request to leave early, and is not going to try to keep you in a lease against your will. The last thing most landlords want to do is chase a defaulting tenant through the legal system, so they will usually try to find a replacement tenant as soon as possible. In a fluid rental market, landlords can usually find tenants. In cases where the landlord has to drop the rent in order to attract a new tenant, you might be asked to make the landlord whole through the end of your lease term.

Again, the most important factor is a good relationship with your landlord. Your landlord does not have an obligation to let you out of the lease, so approaching the landlord in an angry or demanding fashion is likely to be unhelpful, and could result in you ending up in court, a black mark on your credit, and a landlord who will not be at all a good reference for you in future leases. But if you resolve the situation fairly with your landlord, you can save yourself, and the landlord, both money and hassle.

Holding Over After Your Term

Most leases are for a fixed term, such as for one year. What happens when the lease ends, but you’re not ready to move out? That is, you don’t want to stay for another full year, but you need another month or two until your new place is ready. Or perhaps you are sure you do not want another full year, but you’re still looking for a new place.

In practice, when tenants stay beyond their lease, they become a “holdover tenant” under a month-to-month term. If you stay past your term, pay the monthly rent, and your landlord accepts that rent without objection, you can stay on that month-to-month tenancy paying the same rent you were paying during your lease. Sometimes, the lease will specify a higher rate of rent for holdover tenants, so you should look for that term in your lease. It is not unreasonable for the landlord to ask for a higher rate, but sometimes the leases specify a punishing increase in the rent to discourage holdover tenants. Make sure you check for that in the lease.

Also, be careful that you do not get trapped into staying longer than you wish. If you stay even one day beyond the term of your lease, you immediately become a month-to-month tenant who is liable not just for that month’s rent, but also the next month’s rent. And if you do not give notice by the end of your current month of your intention to vacate at the end of the next month, you will be liable for yet another month. That is, if your lease ends September 30th and you hold over, you are liable for October and November’s rent at the same monthly rate you were paying. If you then give notice of your intent to leave by the end of November, your month-to-month lease ends on November 30th. But if you do not give notice until October 1, technically you are responsible for the rental obligations through December 31st.

As always, if you are fair and honest with your landlord, you can probably negotiate a fair short-term rental at the end of your lease. The most important issue to the landlord is having a rent-paying tenant in the property at all times, so if you let the landlord know that you want to stay beyond your lease, but not for another full term, the landlord will probably accommodate you.

Five Ways to Maintain a Great Relationship With Your Landlord

Keeping good relations with your landlord is crucial for ensuring a good experience as a tenant, as well as giving you a great reference for future rentals. Here’s how to keep a great relationship with your landlord.

Although Better Homes and Gardens Realty is only involved in the initiation of your rental process, and not for your actual rental term, we thought it would be helpful to provide you with some information that might give you a better experience once you are actually renting your new home.

Most significantly, we want to counsel you to try to keep a good relationship with your landlord. We see too many situations where landlords and tenants end up in disputes that could have been avoided by both parties acting in and expecting good faith. That’s unfortunate, particularly because of the long-term importance for you in maintaining a good relationship with that landlord.

For example, if you’re planning on renting in the future, any prospective landlord is going to want to know where you’ve rented previously, and you’re going to want your current landlord to act as a reference for you, to attest that you are a good tenant. Also, you never know whether you might need a favor from the landlord, either because you want to terminate the lease early or stay a little longer than your term. If you have a good relationship with the landlord, you’re likely to get that favor, but if you’ve needlessly created disputes with the landlord over minor issues, then you’re not likely to get any accommodation to your needs.

To then end, we wanted to provide you with seven key principles for maintaining a good relationship with your landlord.

- Pay your rent on time.

Nothing will sour your relationship with your landlord more than being chronically late with the rent. Remember that your landlord is basically an investor who needs to maintain cashflow from her real estate investments. She probably has a mortgage on the property, taxes to pay, maintenance bills to pay, and she needs your rent in order to pay her own obligations. It’s simply not fair to be late with the rent. Even if you are having an issue with the space, you should pay your rent on time and work to get the landlord to resolve your issues. If the issues are so serious as to compel you to terminate your lease, then you will have to resolve that, but unless you’re at that point you should pay the rent on time. - Communicate in good faith with your landlord.

Most landlords are good people who will treat you in good faith. Unless your landlord gives you reason to believe otherwise, communicate requests and problems as if you expect that landlord to be fair with you. When you have a problem – with the neighbors, with an appliance, with heating or cooling, with pests, or whatever – communicate it in a non-threatening manner and expect the landlord to help you. Similarly, if you do have a problem making your rental obligations, don’t just hide from the landlord and duck any calls that come in. Be upfront and explain your situation, and hope that the landlord can work out an arrangement for you. - Act in good faith as well.

When you’re living in someone else’s property, you have an obligation to treat it well. Landlords keep security deposits because every landlord has had an experience with tenants who leave a property in terrible shape: filled with garbage, with broken appliances, and scuffed up walls beyond normal wear and tear. Treat your rental as if you own it, and you will get your security back. Similarly, be a good neighbor to the people who live near you. If you are a difficult tenant, the neighbors can create a hassle not just for you but for the landlord. The landlord does not want to have to deal with that. Again, a good relationship with your landlord is in your long-term best interest, so be fair. - Cooperate with agents when your lease is ending.

At some point, your lease is going to terminate, and your landlord is going to need to get a replacement tenant in the space. When that happens, your lease will probably require you to make the property available for show to prospective tenants. Try to be cooperative in that – make the property available, keep it reasonably clean and neat so the potential tenants can imagine themselves living there. You have no particular stake in the property getting rented after you leave, but it’s good karma to be nice to the prospective tenants, the same way you would want fair treatment when you look at rentals. - Don’t skip out on your obligations.

At some point, you may find yourself needing to terminate your lease early, either because you need to move or your can no longer afford the rent. If that happens, approach the landlord openly about the situation. Most landlords will allow you to terminate the lease early if (1) they can get a replacement tenant quickly, and (2) you are open to covering the lease obligations until they do. Skipping out on the rent is going to hurt your reputation in the long run, and it’s simply not necessary when landlords will work with you to try to limit your exposure and get a new tenancy in place.

At Better Homes and Gardens Rand Realty, we work with both landlords and tenants, and we tell both sides the same thing: act in good faith with each other, and keep up a good relationship. It’s better for everyone in the long run.

Understanding Your Lease

When you rent property, you’ll be signing a formal lease, which is a legal agreement between you and your landlord. Because most leases are form agreements, you should be able to prepare for your review of the lease your landlord will provide.

A lease is a formal legal agreement that sets out your obligations to the landlord, and your occupancy rights in your new home. Accordingly, you should make sure to review your lease carefully, and if you are confused about something or concerned about a term you should consult with an attorney.

Leases do not necessarily need to be in writing, but most landlords will require a written lease that sets out the rights and obligations of both parties. Most non-professional landlords use some sort of form lease that is available for sale online or in office supply stores, but professional landlords might have their own lease that they have written themselves.

In either case, most leases have fairly common terms in them to address your legal rights and obligations, so it would be helpful to familiarize yourself with the major common issues.

Common Lease Terms and Issues

Here are some common lease terms, more or less in the order in which they are generally presented in standard lease forms.

Conveyance

The lease should formally state that the landlord is giving you the right to lease the premises, and you’re accepting the premises. This can be as simple as “Landlord agrees to let, and Tenant (Lessee) agrees to take” or can be more formal. Technically, this is called the “demising clause,” but it really just sets out the basic agreement that you will be leasing property from the landlord.

Property description

The lease should clearly indicate what property you are leasing. A street name description is fine. You should just check that you are signing a lease for the correct property, including the unit number for a condo or apartment.

Statement of the term.

The lease should identify the term of the lease. Most written leases are for a fixed period of time, usually set out in yearly increments: a one-year lease, a two-year lease, etc. Essentially, you have the legal right to occupy those premises during that period of time.

Right to Renew

Some leases will contain a provision allowing for your right to renew at the end of your lease, either at the same rental terms or perhaps for a slight increase in the monthly rent. Usually, the term will require you to give notice of as much as three months’ before the end of your lease, to give your landlord time to find a new tenant. If you exercise the right to renew by giving that formal notice (usually a letter to the landlord), you can get another full term. Even if you don’t exercise the renewal right, or if your lease does not have a right to renew, you can always negotiate with your landlord for a new term.

Utilities

The lease should specify who is responsible for the utilities. In most cases, you will be responsible for cable bills, electricity, and perhaps heating. It’s often difficult for the landlord to assign responsibility for water usage, so water might be included within your general rent payment. Whatever the case, you should be aware of whether you will have utility obligations. If so, you might want to see some utility bills for the property to get a sense of how much prior tenants have spent for electricity and heating.

Specification of the Rent.

The lease should state what the rent is and how you are supposed to pay it. The lease will probably state that you need to pay the rent for the month in advance, often at the beginning of the month. Most leases are paid monthly, with the monthly rent amount fixed through the term of the lease. The lease might also contain some sort of penalty if you pay the rent late. A penalty clause is not unreasonable so long as it is within 10% of the actual rent payment; anything more than that is unusual and could be challenged.

Usually, landlords will require the first month’s rent in advance. It’s also common for the landlord to collect both the first month’s rent and the final month’s rent in advance, in order to protect against tenants who decide to withhold the last month’s rent in order to force the landlord to use the security deposit to cover it. Landlords try to avoid that situation, because they need the deposit to cover damage to the property, so they get the last month’s rent in advance to ensure that it gets paid.

Duty of Repair

Most leases will put the duty of repair on the landlord, at least for major appliance repairs and items such as the plumbing, electrical, heating, and roof integrity. It generally should not be the tenant’s responsibility to cover basic repairs and maintenance, at least not in a one-year term, unless the tenant abuses the property and causes the problem. You should carefully review your lease to see whether you have an obligation to maintain basic systems beyond using an ordinary standard of care allowing for normal wear-and-tear. If you do have a significant repair obligation, you might consider negotiating on that point.

Landlord Right of Entry

Most leases give the landlord a limited right of entry on the premises to make repairs, show the property to new tenants during the final months of the lease if you’re planning on leaving, or in cases of emergency. Remember that a leasehold is a legally significant property interest that you have – when you rent the property, you get the right to live in the property, and the landlord loses that right. Generally, the landlord should not be allowed onto the property unless you request it, repairs are needed, or the landlord has some urgency. Unless there is an emergency, your lease should allow for fair notice if the landlord is going to enter the premises. After all, during the lease, it’s your property.

Cooperation with Re-Letting

Your lease might have a term requiring you to give the landlord (or real estate agents) entry during the final several months of the lease for the limited purpose of showing the property to prospective tenants who will take over when your lease ends. This is not an unreasonable request, but you are entitled to advance notice of any showings, and to be present at showings.

Right to Have Pets

The lease might specify your rights to have pets on the premises: allowing for pets, forbidding all pets, or allowing certain types of pets but not others. If having a pet is important to you, you should pay careful attention to any language in the lease relating to pets. Moreover, that’s something you should make clear to your agent when you start looking, because landlords forbidding pets will usually make that stipulation when they put properties on the market.

Delivery

The lease might specify whether the landlord has an obligation to deliver the premises on time. Sometimes, a landlord will sign a lease with a new tenant, then find that the old tenant has not yet vacated. You should require in your lease that payment will not be made until delivery of the premises is ready, which means that the premises are cleared out of other tenants, and broom-swept clean. You should not sign a lease that disclaims any obligation of the landlord to provide for delivery of the premises. It should the landlord’s responsibility, not yours, to free up the space.

Security Deposit

Most leases will provide for a security deposit to provide for payment in the event of damage to the premises, usually one or two months’ rent. What most tenants don’t know is that the landlord is required to hold your security deposit in a special escrow account, rather than commingling it with all the landlord’s other funds. Indeed, if you are renting in a building with more than six units, the landlord is required to notify you where the money is going to be escrowed. You should pay careful attention to any language indicating what the security deposit can be applied to. It should be limited to damage to the property or unpaid rent, but sometimes leases can allow for a more expansive right for the landlord to keep the deposit.

Right to Sublet or Assign

A “sublet” is a lease between the tenant and a new tenant. In a sublease, you as the tenant essentially become the “quasi-landlord” for your tenant, although you remain subject to all the obligations of your lease with the real landlord. This is different from an “assignment,” in which you literally give your rights and obligations to a new tenant, who becomes the actual tenant for the landlord and leaves you free from the lease obligations.

Most leases will have language governing the right to sublet or assign, if only because if the lease fails to address the issue you automatically by operation of law get an unfettered right to sublet or assign. Usually, if the lease addresses the issue, it will give you a limited right to sublet or assign the space to a new tenant so long as you give notice to the landlord and get the landlord’s consent. In a residential lease, the landlord must give consent if your sublet/assignment tenant is a reasonable substitute for you.

Signature Lines

Although leases do not have to be in writing, or be signed, your lease will probably be signed as a matter of good practice. You don’t generally need notarized signatures.

Understanding the Rental Process

Although renting a home is not nearly as complicated as buying a home, it’s still important for you to have a full understanding of the rental process so that you can be prepared for what you’re likely to experience. The process starts with a set of forms and agreements that you need to complete, and ends with the signing of your new lease.

In order for you to have the best experience possible, it’s important for you to understand the rental process, everything from the initial documentation you need to complete, to the search process, and finally to signing your new lease. We’ve identified five steps in the process:

Step One: Signing Rental Documentation

When you meet with your Better Homes and Gardens Rand Realty agent, you’ll be asked to complete a set of legal disclosures and forms to get you started in the process. These forms include:

- New York State Agency Disclosure. This form is required by New York State law to ensure that you understand that we will be representing you as your fiduciary tenant’s agent, looking out for your best interests.

- Disclosure Agreement. We provide this form so that you understand the legal ramifications of renting a home, and the limits of our representation of you.

- Representation Agreement. This form is required by the REALTOR Code of Ethics to ensure that you understand the scope of our representation of your interests.

We recognize that some companies will take out tenants to look at rentals without completing the necessary paperwork, but that’s not the way we run our business. Renting a home is a significant decision with legal obligations and rights, and you deserve a professional approach for helping you find your new home. If other companies do not require documentation, that’s a good sign that you’re not likely to have a professional experience with them.

Step Two: Fill out Your Rental Application

Once we have completed the legal disclosures and established our relationship with you, we now need you to fill out a rental application and credit check authorization. The rental application is a standard form that contains all the information that most landlords will require before considering an offer to lease their property, and will be provided to them as part of an offer to rent. Similarly, the credit check authorization is necessary so that landlords can be assured that you are a reasonable credit risk. Most landlords will not rent to prospective tenants who have not completed a rental application and credit check.

Step Three: Search for your Rental

Once you have your documentation completed, you need to communicate all your needs, goals, and wants for your rental to your agent, so we can narrow down the inventory to show you only what might actually interest you. In discussing your needs with your agent, you should consider the following:

- How much can you afford? The basic guideline is that you should dedicate about 25-30% of your monthly gross income (before taxes, social security, other recurring debts) on your monthly rent. If you want to start saving to buy a home, you can rent under your means and put the savings away for a down payment. And if you want to stretch a little for a perfect rental home, you can try to do that, but your landlord might be cautious about renting to someone who is spending more than 30% of income on housing.

- How long do you plan on staying there? Most tenants prefer a one-year lease term, because one of the reasons they are renting is to retain flexibility and mobility. But if you plan on staying longer, you can propose a multi-year lease. Most landlords are open to longer-term leases.

- Where do you want to live? Renting a home is about becoming part of a community (and a school district, if that’s important), so you need to decide what town or village you wish to live in. Most areas of our region provide for rental housing, so you should have enough inventory to choose from. But you should educate yourself about the community choices you have, and communicate those preferences to your agent.

- What type of home? Most tenants rent a condominium or apartment unit, but in today’s rental market you’ll find many options for single-family homes. The single-family homes are more expensive, and might require more maintenance, but they do provide more room and a home-like feel.

- Do you have any special needs? If you have specific needs for housing, such as bedroom needs, pets, mobility issues, or anything else that might be unusual, you should make sure your agent knows about it so that we can provide you options that meet those needs.

Your agent should ask you these questions when you meet, but you should be proactive and engaged in making sure you communicate all your needs so that we can better service you.

Step Four: Shopping for a New Home

The next step is the fun part – shopping for a new home. Your agent should provide you with a comprehensive list of all rental properties that meet your price range criteria and your particular needs. Now it’s just a matter of going to actually view the properties.

Here are some guidelines for viewing potential rental properties:

- Does the current tenant express any opinion on the property, or of the landlord?

- Is there adequate parking for your needs?

- Is the condition of the property suitable?

- Is the property convenient for your commute, shopping needs, or school needs?

- Will you need additional or new furniture for the new home, and can you fit your current furniture in the room layouts?

- What do you think of the neighborhood?

- If it’s a complex, what do you think of the layout of the complex, the other tenants, and what it would be like to live there?

Ultimately, deciding where you want to live is an intensely personal choice. Your agent is there to assist you and answer your questions, but the decision is up to you.

Moreover, you can do a lot of searching on your own. Although your agent should be providing you with a comprehensive list of available properties, you can always register with RandRentals.com to view properties on your own. The site features include:

- Client registration, so that you can save properties on a “wish list.”

- Comprehensive search ability to look for rentals by area and by a narrow price range suitable for rentals.

- Community information for all local areas.

- Full pictures and descriptions of all rental properties available.

- Mapping of all properties.

You can always find potential properties on your own, then email them to your agent to arrange a showing. As always, the more engaged in the process you are, the better an experience you’ll have.

Step Five: Signing a Lease

Finally, once you have identified the right new home to rent, you’ll need to make an application to the landlord and sign a lease. Before you sign that new lease, though, you should make sure that you and your agent have done some basic due diligence on the property and the landlord:

Have you inspected the property?

You don’t need a formal home inspection, although for a long-term lease we recommend investing in a thorough inspection to ensure that your tenancy will not be subject to vermin infestations or structural and appliance breakdowns. Even without a formal inspection, you should check electrical outlets, flush all the toilets, make sure the appliances work, and run the hot water in the showers to check temperature and water pressure.

Have you spoken to other tenants?

If you’ve had the opportunity to meet the current tenant, you might ask about their rental experience and their relationship with the landlord. Or you might be able to meet other tenants in the complex, or other tenants of that individual landlord. Just keep in mind that opinions by tenants can be skewed by their particular experience, so issues they have might be more their own rather than the landlord’s.

Is the landlord reliable?

Most people think of reliability issues in leases as involving a tenant who might default. But it’s a good idea to check whether the landlord seems like she is solvent and able to maintain the property, simply because if the landlord ends up in default on her own obligations to her bank, she might get foreclosed on. A foreclosure would terminate your existing lease, and leave you without any right to occupy the property. One way to ensure that your landlord is solvent is to take advantage of Better Homes and Gardens Rand Realty’s affiliate services program. Our title company, Hudson Abstract Services, can do a simple lien search on the property to determine whether the landlord is currently facing foreclosure. We provide that service as a complimentary service to clients who obtain renter’s insurance from our affiliate Hudson Group Insurance.

Finally, if you are satisfied that this is the right place for you, then it’s time to sign the lease. Most likely, your landlord will provide you with a form lease that can be purchased online or at office supply stores, so you will know that the terms of that lease are fairly standard. If you want to know more about the common terms in a residential lease, make sure to read Understanding Your Lease, which explains all the basic terms and what to look for.

Getting Renter’s Insurance and a Free Lien Search

Your landlord has insurance, and so should you. If your rental property burns down, your landlord has coverage to protect her investment. But if you lose everything you own, you’re generally not covered unless you get something called “Renter’s Insurance.” Renter’s Insurance is a necessity for anyone renting or subletting a home or apartment. Whether you live in a single family home, duplex, townhome, condo, loft, studio or apartment, you should get renter’s insurance to protect your belongings and your liability. For less than a dollar a day, a renter’s insurance policy will cover all of your property at its full replacement cost.

Even better, if you get renter’s insurance from our affiliate Hudson Group Insurance, we will provide you with a free lien search on your property to ensure that your landlord is not facing imminent foreclosure that would terminate your lease after you move in. That’s a free service we provide to all Hudson Group Insurance Clients.

If you’re interested in getting Renter’s Insurance, just call 845-215-0173

Five Good Reasons to Rent, and Five Good Reasons to Buy.

At Better Homes and Gardens Rand Realty, we help thousands of renters rent their new homes each year. We also help thousands of buyers purchase a home. The decision on whether to rent or buy is a very personal one, but it’s important to understand when one choice might be right for you.

Traditionally, most people have thought of of renting as the temporary stop on the way to home ownership. After all, home ownership is part of the “American Dream,” and even with the recent turbulence in the housing market remains one of the best ways to plan your financial future.

But we have certainly seen perspectives on renting change in the past few years, as renting becomes a much more viable option for many people. Maybe it’s because people are simply spooked by the decline of the housing market in the middle of the last decade. Maybe it’s that rental options are better than ever, because more good rental housing is coming on the market as homeowners opt to wait out the market before selling by renting. And maybe it’s just because a younger generation coming into the housing market is less likely to set down permanent ties by buying a home, since people get married later, have kids later, and tend to change jobs more than in their parents generation.

At Better Homes and Gardens Rand Realty, we work with thousands of tenants every year with the goal of giving them a great experience in renting their new home. We believe that renting is a great option for some, which is why we have made the commitment to renters by creating RandRealty.com, a dedicated site for rental search and information, as well as a whole series of service systems to take great care of rental clients.

At the same time, we also believe that the best long-term financial decision most people can make is to ultimately purchase a home. So even if buying is not in your immediate plans, we want to make sure you’re aware of the pros and cons of renting versus buying so that you can make an informed decision about which choice is right for you.

Accordingly, we have provided five good reasons to rent, as well as five good reasons to buy.

Five Good Reasons to Rent

Here are five good reasons to make the decision to rent a home:

- You want to maintain flexibility and mobility.

We are living in a “mobile” age where people like to keep their options open. People get married later in life, and have kids in their thirties rather than their twenties. Few people, even those that love their jobs, believe they’re going to work for the same company for their whole careers. If you’re in that kind of situation, it makes sense to keep some flexibility on where you live. If you buy a home, you will find that mobility constrained by having to sell home before you can transfer to that new job, move in with a new significant other, or make any other life changes. - You need to repair your credit history.

Another unfortunate consequence of the recent economic difficulties of the last few years is the number of people with blemishes on their credit history. People with low credit scores can find it very difficult to buy a home, so even if it’s in your long-term plan to purchase, you can spend time renting while your credit history recovers. It can take several years for certain credit problems to work their way out of your file, and during that time you can reestablish your creditworthiness. - You need to save for a down payment.

Today, many people opt to rent even when they have the resources for a down payment to purchase. For many, renting is the short-term solution for their housing needs while they save up for a down payment. If your long-term plan is to purchase, then renting in the meantime while you save up for a down payment (or a larger down payment) is the right choice. - You have other places to invest your money.

Even though real estate is still a good long-term investment, despite the experiences of the past few years, it’s not the only good long-term investment. People in the financial services industry, for example, often forego purchasing even if they can afford it, because they have an expertise in other investment products in which they believe they can get a better return. If that’s your situation, and you believe that you could personally invest your savings and get a better return elsewhere, then renting is a good option for you. - You are risk averse.

Finally, some people opt to rent because they simply do not want to take the risks of investing their money in real estate, even their own real estate. This is not a position we agree with, specifically because we have seen the long-term investment potential of real estate in our own lives and in the lives of our clients. But we can understand how the experiences of the past few years have spooked potential buyers into becoming renters. If you’re simply averse to putting your money at risk when you could get lower but safer returns with other investments, then renting is a good option for you.

Saving for a Home

One good way to accelerate your plans to purchase is to rent below your means, and put the difference between what you pay and you could potentially afford into a savings account dedicated to your down payment. The general guideline is that you can afford to spend about 25%-30% of your gross monthly pay for your rental costs. But if you were to only spend, say, 15-20% of your income on your rental, and rent something a little less costly, you could afford to put away hundreds of dollars a month toward your down payment.

Remember that it doesn’t take much. Homes can be purchased in our area for as little as $150,000, and federally-insured loan options are available for as low as 3.5% down, so you could potentially purchase a home for as little as $6,000 plus another $2,000 or so for out-of-pocket closing costs.

Five Good Reasons to Buy

We would not be doing our job as real estate advisors if we did not at least highlight some of the reasons why most Americans own their own home. While renting is a great option for some, there are also good reasons to purchase a home. Specifically, if you are making the decision to rent, you need to make sure you understand that you are foregoing some of the financial benefits of home ownership.

- Building investment equity over time.

The biggest reason to own rather than rent is the ability to build equity. After all, one of the reasons your landlord owns the property you’re going to rent is that you are going to help her build equity in her property by paying down her mortgage. Millions of Americans have solidified their financial future by owning their own home, and gradually paying down their principal month by month until they have significant equity that can be liquidated for other investments or for retirement. Although you don’t build equity quickly on a new mortgage, since most payments go toward interest at first, over the first seven years you will pay down about over 10% of the principal. On a $300,000 loan, that’s $30,000 in equity built over just seven years. - Leveraged Appreciation.

Most people understand the concept of appreciation – the increase in value of an investment over time, such as when a stock goes up in value. But most people forget that appreciation in real estate is leveraged appreciation. For example, if you buy $20,000 of stock, you own $20,000 in stock. If the stock appreciates by 10%, you now own $22,000 of stock, since 10% appreciation of a $20,000 investment is $2,000.But when you invest in real estate, you put down $20,000 to buy a $100,000 home (with 20% down). If that home appreciates by that same 10%, the home is now worth $110,000. But the return on your investment is not just 10%, because you are getting leveraged appreciation. You only put $20,000 into the home, so the $10,000 return is actually a 50% return on your $20,000 investment (i.e., $10,000 is 50% of $20,000). - Tax Deductions.

When you rent a home, the rental payments you make are not tax deductible. But when you own a home, you get to deduct the full amount of the interest you pay on your home mortgage from your federal and state tax income. For example, if you get a $300,000 mortgage at 5%, you’ll make about $20,000 in payments in the first year, of which about $15,000 will be tax-deductible interest. That interest comes right off your income as a deduction, so if you are at an income level where you pay 28% federal and 6.85% New York State, you save over one third (28% plus 6.85% is 34.85%) of those interest payments because you will not pay taxes on that. That would be a savings of about $5,000 on your $15,000 in interest payments. (Although there is talk in Washington about reducing the mortgage interest tax deduction, it seems unlikely that much will change for all but the highest income taxpayers.) - Homes are now well-priced in our area.

The market in our area is for sale at about 25% less than buyers were paying five years ago, and prices are now back to 2003 and 2004 levels, well before the frenzy of the irrational seller’s market of 2005-06. We believe that homes are a good value right now, and while prices may not go up in 2011 or 2012, over time we will start to see appreciation. There’s a reason they call it a “buyer’s market,” because buyers can find good opportunities when inventory is high, demand is low, and prices are down. - Interest rates cannot stay this low forever.

People fail to appreciate how much impact interest rates have on home values. As we write this in the middle of 2011, we are seeing rates still remain at historic lows in the 5.0% range and prices down 25% from their highs. That is a powerful combination. Even if prices were to come down a little more, it only takes a half-point increase in interest rates to make homes more expensive than they are right now. Essentially, every half-point increase makes homes about 5-6% more expensive – either by making your payment 5-6% higher, or lowering your maximum purchase price by 5-6%. People who decide to wait to purchase until prices come down might not save themselves anything if rates go up.

All that said, the decision to rent or buy is an intensely personal one. Our goal is to simply make sure you’re informed about that decision, and to give you a great experience in whatever you decide to do.